Is Google Worth Buying at $160?

Why buying Google because of its 20 P/E ratio could be a mistake

In recent months, many investors have flocked to Google, justifying the decision to buy this Big Tech stock simply because it trades at a P/E of around 20.

But as you should know by now, multiples require nuance—they’re not the best tool for valuing a stock.

A P/E of 20 doesn’t offer much without context, and Google, in particular, needs that context. In this post, I’ll walk you through my process for analyzing Google, with the goal of deciding to buy or not.

What You’ll Read Today

Google at a Glance

Moat

Valuation

Google at a Glance

When I say Google, of course I’m referring to Alphabet, its parent company. This post isn’t a deep dive, but understanding how the company generates revenue is still important.

Alphabet is segmented in three main segments, with Google Services further divided into multiple pieces:

Google Services

Google Search

Google’s lifeblood, the core product and by far its largest revenue driver. As the world’s most popular search engine, it handles trillions of searches each year. Revenue comes from advertising, with various ad solutions generating over $198 billion in 2024.

YouTube Ads

One of the best acquisitions in history—Google acquired YouTube for $1.65 billion in 2006. In 2024, the platform generated over $36 billion in ad revenue, and is now the leading streaming service on TVs, surpassing even Netflix.

Google Network

This segment includes ads placed on third-party websites and apps via AdMob, AdSense, and Google Ad Manager. If a website or app wants to monetize through ads, it can use Google’s services to display the most relevant and profitable ones. While growth has stalled, this segment still generated over $30 billion in 2024.

Subscriptions, Platforms, and Devices

A mixed bag of products and services, including:

YouTube subscriptions (YouTube TV, YouTube Music, YouTube Premium)

The Google Play Store

Pixel devices and other hardware

Together, these generated over $40 billion in 2024.

Google Cloud

Google’s cloud computing division, offering storage, computing power, and other complementary products. It competes with AWS and Microsoft Azure and is growing rapidly, generating revenue of over $43 billion in 2024.

Other Bets

A collection of moonshots projects—high-risk, high-reward ventures. The segment generated $1.6 billion in revenue, mainly from healthcare-related services (likely Verily and Calico) and internet services. The most notable business in this category is Waymo, Alphabet’s self-driving technology unit.

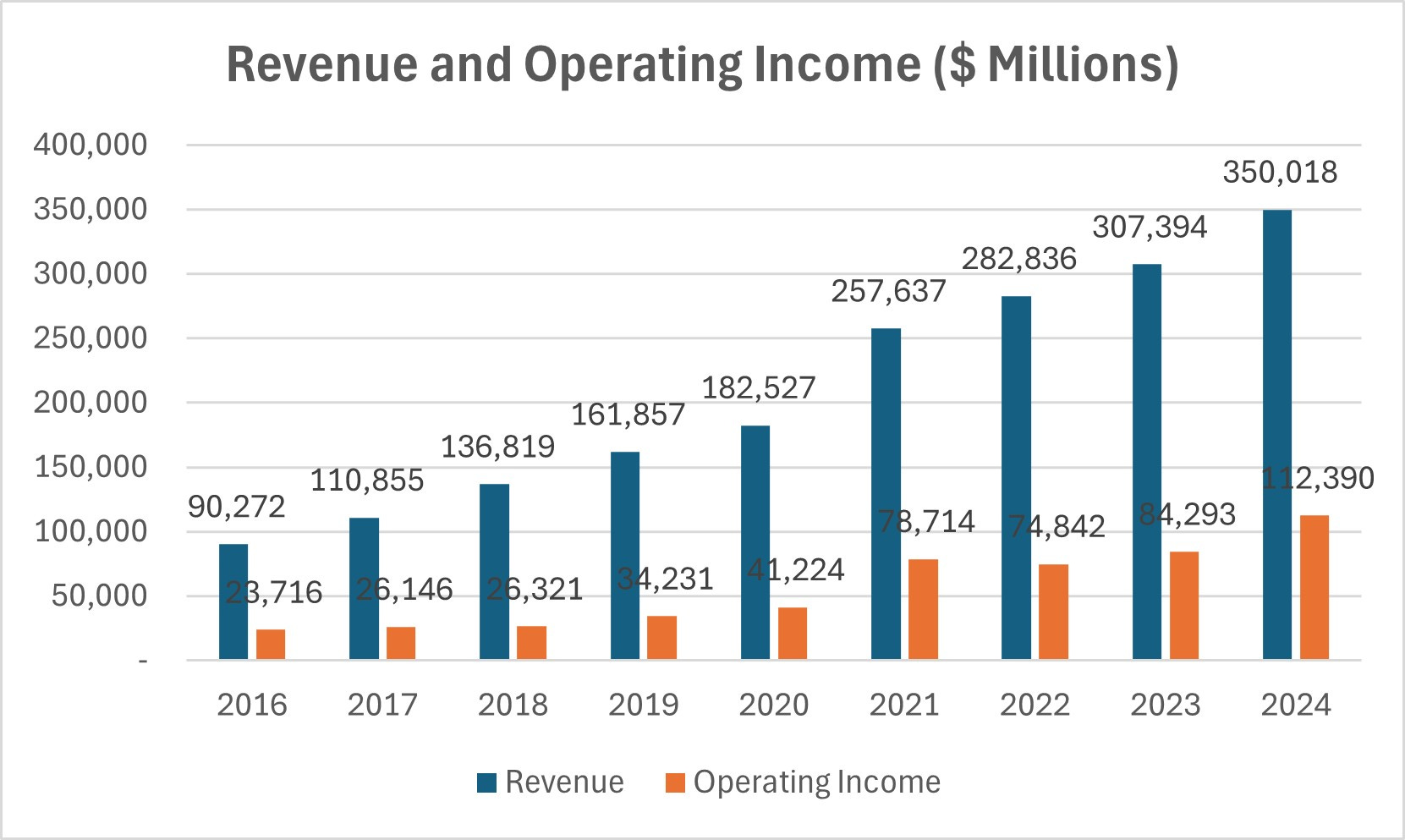

In 2024, Google generated $350 billion in total revenue, while operating profit reached $112 billion.

Moat

Google’s competitive advantages are undeniable. Google Search is the most powerful and widely recognized search engine, fueled by massive amounts of user data that continuously improve both the product and its advertising capabilities. YouTube dominates online video with clear network effects, while Google Cloud is one of the big three cloud businesses. Google’s ecosystem—including Android, Chrome, Gmail, Maps, and Drive—creates high switching costs and strong user lock-in.

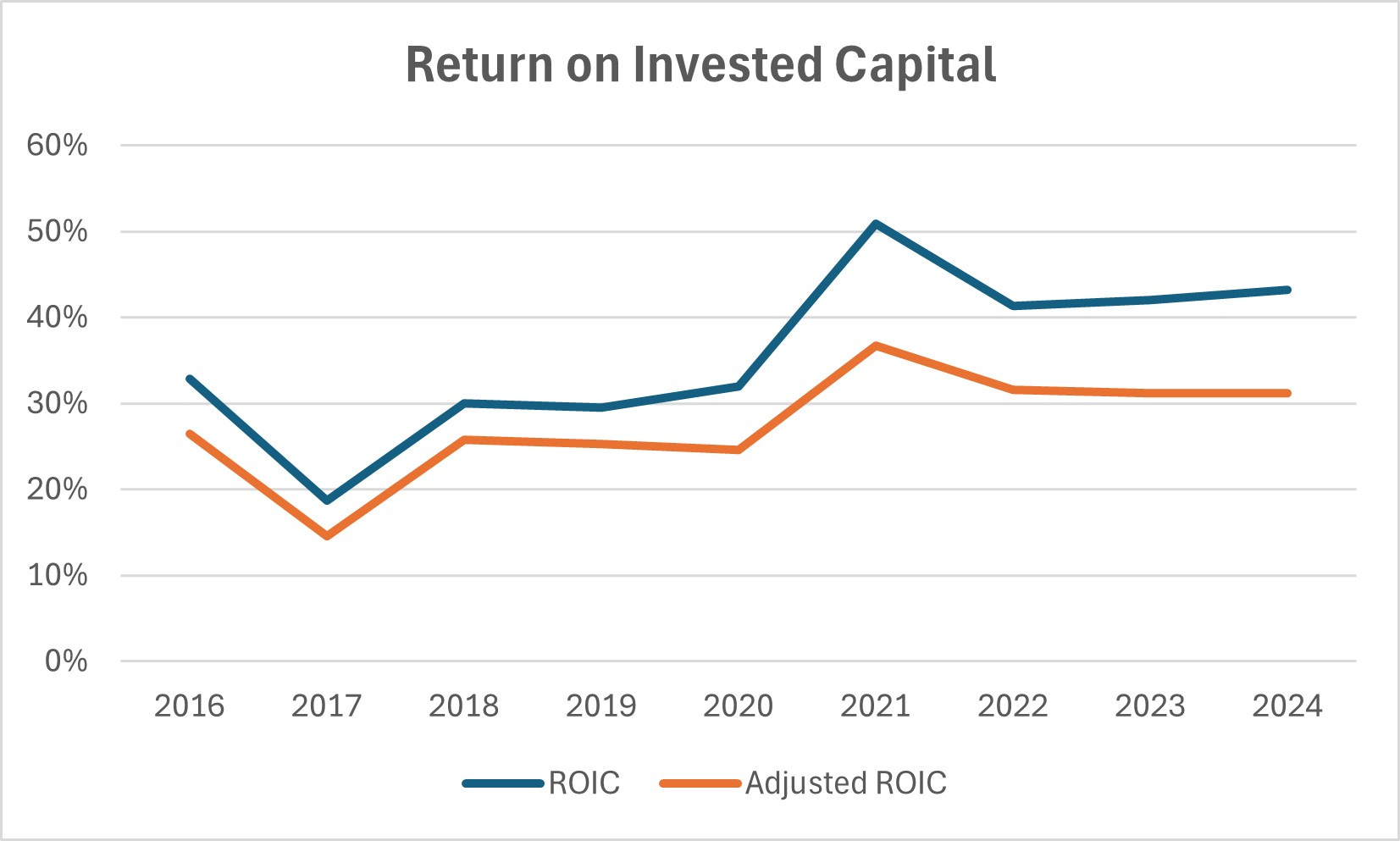

As discussed in my previous post, a strong moat is often reflected in high returns on capital. Even after adjusted for intangible investments expensed through the income statement, Google’s ROIC remains above 30%.

But the big bad hanging over Google’s moat, of course, is disruption in Search, particularly from AI-driven technologies. ROIC, a backward-looking metric, doesn’t capture this risk.

Consumer preferences are shifting toward conversational, answer-focused search methods powered by large language models (LLMs). Ultimately, people turn to Google for answers, but AI often delivers better, more concise, and even personalized responses. Ask yourself: would you rather sift through 10 blue links or receive a direct, well-structured answer?

LLMs enable the latter, and consumers are catching on fast. The adoption of generative AI has been swift, with many consumers already using AI habitually.

So why has Google seemed “slow” in adopting LLMs? Yes, they have Gemini, and AI is being integrated into search through features like AI Overviews. But the real hesitation, in my view, comes down to a lack of incentive. Search is a massive cash cow fueled by advertising, whereas LLMs operate under a different model, less reliant on ads.

That said, AI Overviews, while not directly monetized, are still embedded within search, where ads remain relevant. And with Google’s vast distribution network, its AI products—many still in early phases—are quickly scaling.

If Google Search evolves to offer both conversational, answer-focused AI responses and traditional search results, LLMs from other players could become obsolete for answering queries. By then, LLMs will obviously still have its place, but less so for searching answers. And Google’s reach extends far beyond search—Chrome, Android, and YouTube provide powerful distribution channels.

There’s no doubt Google Search is and has been under pressure. Google is answering by implementing AI in its search engine, and it seems to be working: the company sees more than 5 trillion searches on Google annually.

Many investors use the current uncertainty around Google as an opportunity to buy the stock, stating that the company is cheap based on its P/E ratio. Is this justified or not?

Valuation

I’ll attempt to value Google based on its future cash flows, discounted to today. In this scenario, I’ll assume that Google Search successfully adapts to and incorporates AI, such that consumers turn to Google for nearly every type of query—whether they’re seeking general answers, specific websites, personalized responses, or anything else.

As a result, I assume Search to maintain steady revenue growth despite its size. Additionally, Google’s other businesses, particularly Google Cloud and YouTube, should continue their growth trajectories.

Here are the key assumptions for my forecast:

Revenue grows at a low double-digit rate in the early years, gradually slowing to 3% by year 20. Google Search decelerates more quickly given its size, reaching 3% annual growth by year 10.

Operating margin expands from 32% to 35% over the next decade, then stabilizes.

A constant 20% tax rate, which is historically high for Google.

D&A and capex decline as a percentage of revenue. Capex is expected to be around $75 billion in 2025.

The projection assumes ROIC declines over time, reflecting mean reversion. Returns on incremental invested capital remain above 20% for the first 10 years before trending down to 12% by year 20, marking the end of the explicit forecast period.

Under these assumptions, free cash flow grows from $53 billion in 2024 to $279 billion by 2044, reflecting a 9% CAGR.

To arrive at the valuation, solving for the discount rate at a share price just above $160 results in a 9.3% discount rate. Reasonable, but this doesn’t leave a significant margin of safety—especially given the risks to Google’s business model if Search struggles to compete with LLMs.

Google could be a decent opportunity, particularly if my assumptions prove too conservative. If Search sustains double-digit growth for longer or if ROIC remains high longer, there could be more upside.

What’s clear, however, is that Google isn’t a screaming buy at the current price. A discount rate of 9-10% tells me this stock is roughly fairly valued based on my projection.

The goal of this post was to shed light on Google and why investors shouldn’t base buy or sell decisions solely on a “low” P/E ratio. That’s not valuation—it’s either ignorance or a lack of understanding. Then again, Google might still be a decent opportunity if you believe my assumptions are too conservative.

In case you missed it:

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

Great post. I think the problem with most is they use the "a stock is cheap" argument without taking into account the timeframe of ownership. Google I believe is a buy, but that's from me using a DCF for the next 5 years. The longer you project, the less attractive it is, of course. But time matters.

Quick thoughts: we all know that none of the current AI models make money, and they are all burning money, and it's not going to stop simply b/c of this reason: the subscription model doesn't nearly cover their costs on compute and inference. So, while everyone is talking about how Google "could" be disrupted, no one is talking about how long it would take for the so-called "disruptors" to be profitable and how many more rounds of funds they need to raise.

Who will be the last man standing from this bunch, do we even know? And don't forget what DeepSeek (and there will be many more coming out of China) has done is lowering the costs and entry barriers for more AI startups to compete which will bring down the revenue of these AI companies (Good luck Sam Altman) Google, on the other hand, has a massive war chest at its disposal and is positioned to disrupt itself IF it chooses to, the question is when and how. Google knows the dilemma it currently faces, so it's not like they are waiting to be disrupted