Evolution's Short-Term Weakness Persists

Evolution ($EVO): Q3 results and updated valuation

Evolution’s Q3 report yesterday was one of its most anticipated this year. While Q2 results still weren’t great, there were early signs of improvement. The company’s countermeasures against cybercrime in Asia seemed to be taking effect, North America continued gaining momentum, and management expected Latin America to improve in the second half of the year.

But Q3 earnings were rather weak: revenue declined to €507.4 million, down from €519.4 million a year earlier. Consensus had expected €538 million.

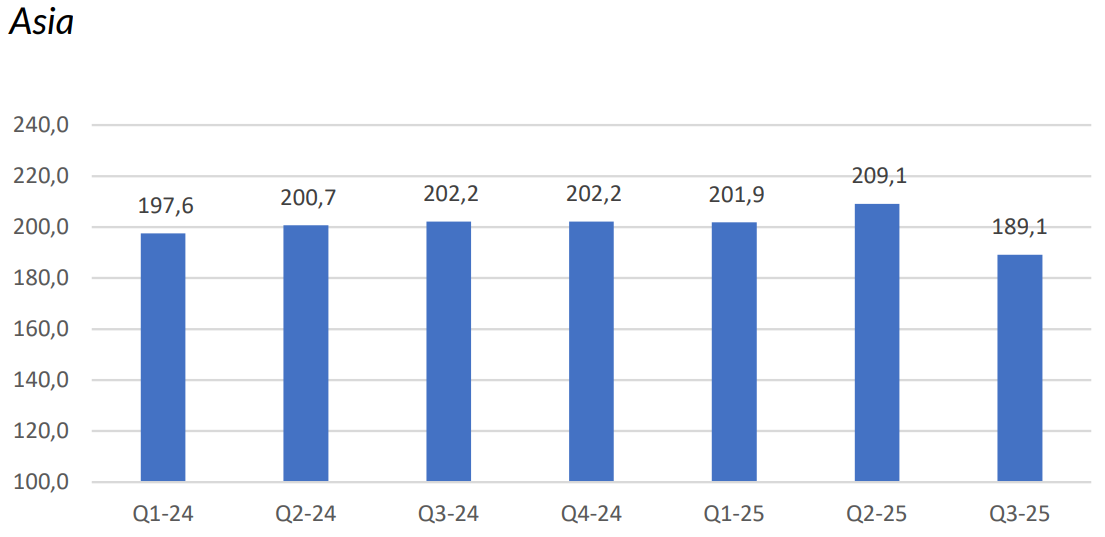

Asia remained the biggest problem region. Cyberattacks continue to plague the business, and Evolution’s countermeasures somewhat backfired as they overreached.

So in other words, the incremental progress seen in Q2 has largely been undone, and the narrative has turned negative again. Still, there are some positives in the report, and management’s commentary adds useful context.

Below is my analysis of Evolution’s Q3 results and my updated valuation.

Revenue Declined but Some Bright Spots

Evolution’s shares have been hammered in recent years. The company remains in a prolonged drawdown, and while the Q2 report suggested the bottom might be near, that now looks a lot less certain.

There’s no denying the valuation is still undemanding, but the stock has been dead money for some time—opportunity cost is the main issue. Even so, I continue to hold shares and am willing to look past the short term.

This quarter, Evolution generated €507.4 million in revenue, down 2.4% year over year and 3.2% quarter over quarter.

For the first time ever, the RNG business outperformed Live. RNG grew 4.1% to €75.5 million, while Live declined 3.4% to €431.7 million. Obviously, Live remains the most important segment by far, but it’s encouraging to see RNG finally gaining some traction.

Evolution operates across four distinct regions—almost like four separate businesses, because each region has a lot of different things going on.

Starting with Asia, the most important but also most troubled region, revenue declined 6.5% YoY and 9.6% QoQ to €189.1 million.

According to CEO Martin Carlesund, this weakness stems from three factors:

Cybercrime: Persistent and widespread cyberattacks continue to disrupt the business. Evolution has struggled with this issue for over a year now, losing meaningful business as a result.

Overextended Countermeasures: The company’s efforts to combat piracy were too severe this quarter, blocking legitimate customers as well. Carlesund acknowledged this, saying:

“I think we are on to it and we are doing the right things. And it’s also natural that there will be a situation where you do too much because otherwise you won’t know where the borders are.”

It’s also worth mentioning that the knowledge Evolution gains from addressing this problem will strengthen its defenses globally. Cybercrime isn’t yet a problem elsewhere, but if it becomes one, Evolution will be better prepared. Once an effective balance is found in Asia, the company should have a new foundation from which to grow.

Regulatory Volatility: Markets like India and the Philippines are in transition. The Philippines recently introduced regulation, creating short-term turbulence as operators and players adapt. India is also moving toward regulation, adding uncertainty.

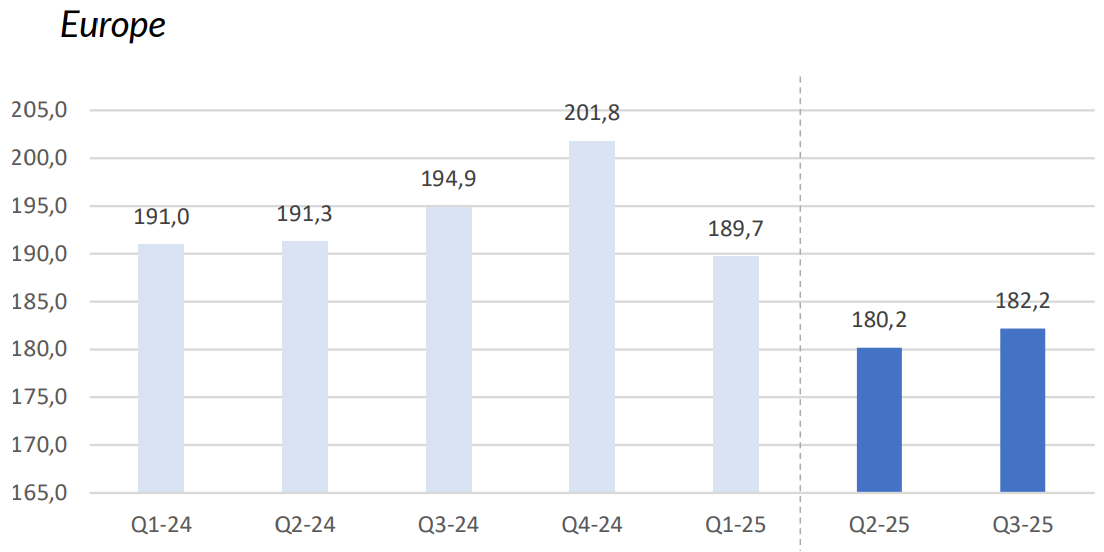

Moving on to Europe, which performed slightly better, and whose outlook is less murky. Revenue reached €182.2 million, down 6.5% YoY but up 1.1% QoQ.

This sequential improvement matters. Earlier this year, Evolution began ringfencing—restricting games to licensed operators only and walking away from grey market revenue. As a result, the company has had to “start over” from a lower revenue base. Q2 was the first quarter fully impacted by ringfencing, so it’s good to see growth resuming from this lower base.

When asked about future growth rates for Europe, Carlesund noted that Europe is already the most mature market but still highlighted historical growth of 9–10% to which Evolution could hopefully return.

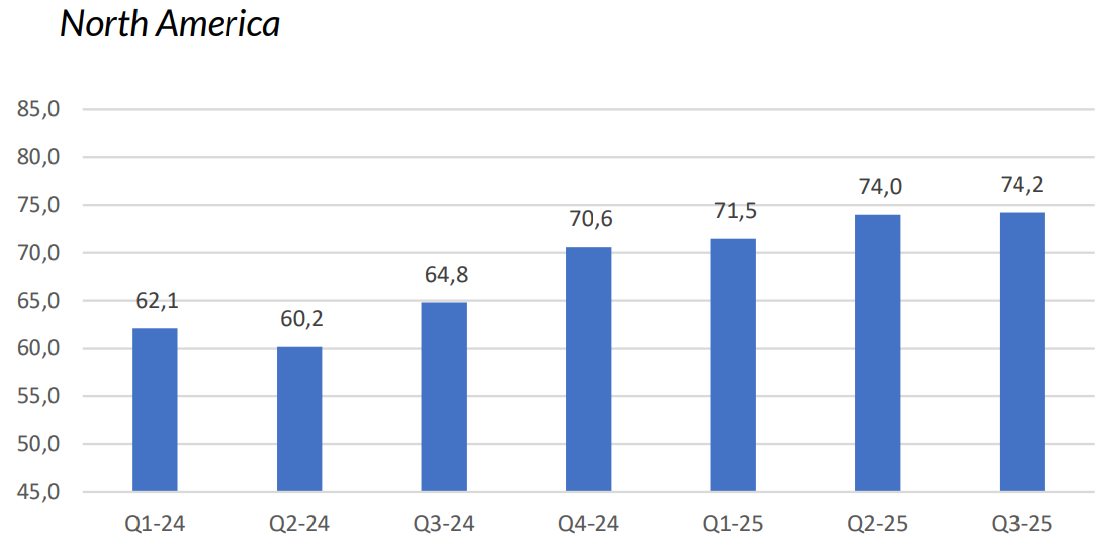

North America largely remained a positive during the quarter: revenue rose to €74.2 million, up 14.5% YoY and 0.3% QoQ.

This is solid, especially given that California banned sweepstakes gambling midway through the quarter, forcing Evolution to exit that small segment. The company also launched its second Live brand, Ezugi, in the US and plans to open a second studio in Michigan in the first half of 2026.

North America remains a long-term growth opportunity, as still only a handful of states have legalized gambling.

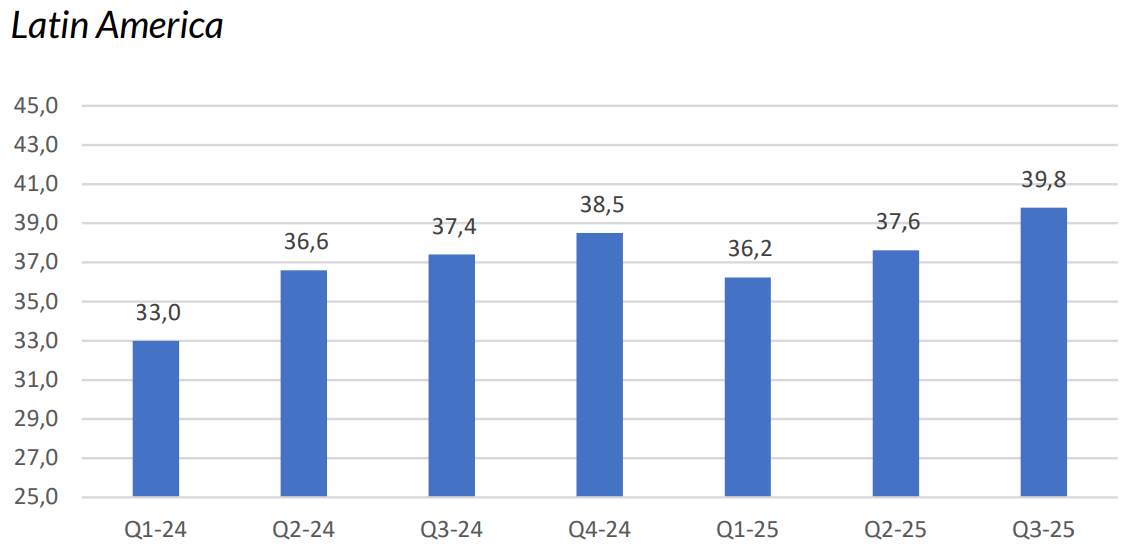

Finally, Latin America delivered €39.8 million in revenue, up 6.4% YoY and 5.9% QoQ.

The new Brazil studio, launched in Q2, is off to a strong start. Management noted that both players and operators are adapting to the new regulatory framework, driving increasing activity.

On a positive note, despite the weak top line, profitability largely held up. EBITDA reached €336.9 million, a margin of 66.4%. Management reaffirmed full-year guidance of 66–68%.

Operating income was €296.6 million, down 21.7% YoY. The sharp drop was due to lower revenue and a one-time €60 million benefit in Q3 2024. Excluding that, operating income declined roughly 7%.

Free cash flow remained strong at €337.3 million, consistent with the long-term trend. Q2 was abnormally low due to seasonal tax payments and working capital buildup.

Overall though, this was still a weak quarter. It’s not easy to keep holding Evolution, but it’s important not to get short-sighted.

The company will never return to its hypergrowth phase, but high single-digit or low double-digit growth is still achievable. Once the Asia countermeasures are optimized—creating a stable base in both Asia and Europe—I can see growth reaccelerate.

Evolution is still learning how to best address the cyberattack problem, and that takes time. Management first mentioned it in Q3 2024, so it’s been only a year. In business terms, that’s nothing. The next quarter is already defined; long-term success is planned over years, even decades.

That said, I still think the current valuation looks cheap. All it may take is a single quarter of high single-digit growth to act as a catalyst. That could be enough to rerate the stock and reverse the negative trend.

With that in mind, here are my current thoughts on Evolution’s valuation.

Should You Buy Evolution Today?

Currently, Evolution trades at a price-to-free cash flow of around 10. That is exceptionally low.

So far in 2025, the company as returned nearly €1 billion through dividends and share buybacks. That equates to roughly an 8% yield. Most investors would be content with an 8% annual return, yet Evolution has achieved that in just nine months through capital returns alone.

Earlier this year, I published a free valuation model for Evolution. It was built on highly conservative assumptions and produced a fair value range of 745 to 1,042 SEK. I still believe those assumptions hold true going forward.

With shares currently around 670 SEK, I view Evolution as an attractive buy. The main risk is that the stock continues to be dead money for a longer time.

If you can tolerate that opportunity cost, anything below 750 SEK remains, in my view, a very good entry point.

Thanks for reading.

Lucas

Author & Founder, Summit Stocks

In case you missed it:

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

Hey, great read as always. Your insight into the countermeasures backfiring in Asia is sharp. What if Evolution deployed more AI-driven cyber defense from day one? It feels like a missed opportunity to prevet those setbacks. Always appreciate your analysys!

The patience test with Evolution continues. The fundamentals remain solid, but the story feels stuck between recovery and relapse. Asia’s setbacks clearly sting, yet the resilience in margins and steady cash flow show a business still built to endure. At these valuations, it’s less about chasing momentum and more about conviction in the long arc. But hey, sometimes holding through the noise is the real edge.