Price Targets for My Portfolio | Pt. 1

Airbnb, Amazon, ASML, Basic-Fit

Summit Stocks will offer a paid subscription tier starting next week. To learn more, check out this post.

As I continue compounding knowledge, I’ve come to realize something important: since the inception of the portfolio I track here on Substack, my buy and sell decisions—and my valuation methods—have often been foggy, unclear.

Recently, I’ve started embracing smarter ways to value businesses, always grounded in one principle: discounting future cash flows to their present value. (Just check out my post last week.) The point is, I’ve learned a lot in the past year about valuation.

I’ve also come to realize that valuation matters more than I first believed. You can’t just hide behind a Warren Buffett quote like the one below and justify buying a high-quality business at any price. It will hurt returns, at least in the short to medium term.

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Frankly, that’s exactly what I did.

That’s not to say I don’t stand behind my buy decisions—I do. I believe the businesses I own are strong and capable of generating satisfactory returns. But in some cases, I wasn’t disciplined enough or knowledgeable enough on valuation. Going forward, that changes.

Today, I’ll take a closer look at the stocks I own—their valuations, and the prices at which I’d consider buying more. In doing so, it might become clear that I overpaid for a few. In the next part, I’ll discuss the remainder of my stocks.

What You’ll Read Today

My Price Targets For:

Airbnb

Amazon

ASML

Basic-Fit

Airbnb

Since going public in 2020, Airbnb’s stock performance has been lackluster, with the stock down nearly 20%. A big part of this can be attributed to an initial overvaluation and overly high expectations. Fast forward five years, and the company’s fundamentals have had time to catch up with the stock price, which has been trading mostly sideways for the past three years.

Key Points About Airbnb:

Airbnb operates with negative invested capital due to negative working capital and low non-current assets. The company collects payments before customers stay, which is booked as a liability. Airbnb holds onto this cash until the customer’s stay is completed, even earning interest on it.

Since Airbnb follows a marketplace model, its tangible assets are minimal. Growth comes from reinvesting in R&D and SG&A, as well as the self-reinforcing network.

Because of negative invested capital, Airbnb has a negative ROIC, making it difficult to use ROIC directly in a DCF model. Negative ROIC isn’t bad in this case (far from it), but it complicates the valuation. The simplest solution here that I can see is to adjust for excess cash in the invested capital, resulting in a positive but dilutive ROIC. This leads to an adjusted ROIC of 24% for 2024.

The next step is defining the forecast period. A few factors need to be considered: Airbnb faces ongoing regulatory risks, but its network is massive, and it remains the clear leader in the alternative accommodations space. The company is still expanding internationally and has plans to introduce complementary product offerings in the coming years.

Given the strength of Airbnb's moat but also the associated risks, I believe a forecast period of no more than 15 years strikes the right balance.

In my model, I start with early revenue projections based on analyst estimates, after which growth slows to 2.5% by year 15. I expect the operating margin to reach 32%, similar to Booking Holdings’ current margin.

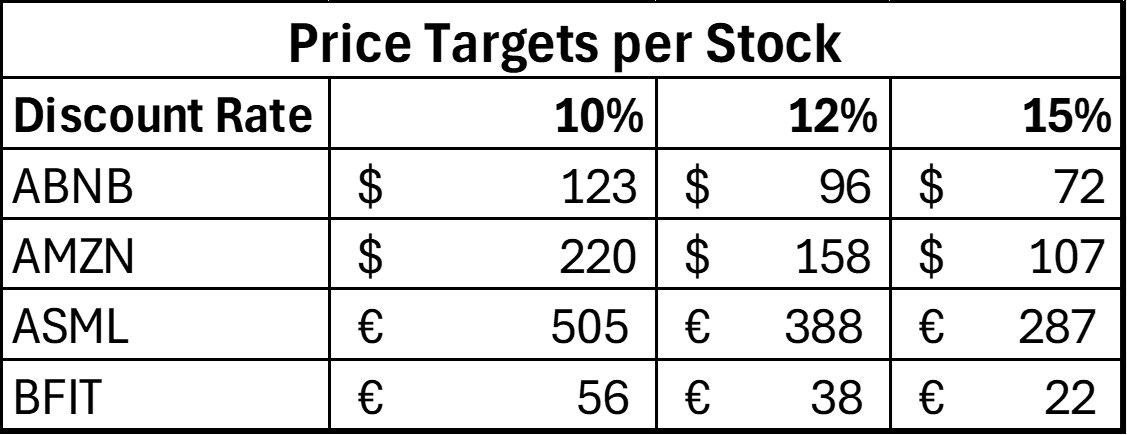

Using a 10% discount rate, my valuation for Airbnb is around $123. This doesn’t account for the company’s interest income, which can and has been significant, given that Airbnb holds substantial cash, including customer funds. At a more conservative 12% hurdle rate, the target price drops to approximately $96, providing an additional margin of safety.

In summary, Airbnb seems fairly valued at its current price based on these estimates.

Amazon

In a post about Amazon a couple of months ago, I wrote:

“Where I first tried to project Amazon’s future free cash flows to assess its valuation, I increasingly realize that it’s a lot more complicated with Amazon … Amazon has never fully optimized for free cash flow generation, and that will not change in 2025. Given the unpredictable nature of its investments, trying to project free cash flow right now feels like pure guesswork …”

I still stand by that. Amazon has never really optimized for free cash flow, and forecasting it is tough. But it’s still worth trying. Being vaguely right is better than not trying at all—getting it precisely right was never an option to begin with.

Amazon’s ROIC in 2024 was about 17%. Since the company has never focused on maximizing profits, I start by projecting a period where ROIC increases, where Amazon finally starts reaping the rewards of its investments, before letting it fade. This requires a long forecast period, one that also reflects Amazon’s deep and durable competitive advantages.

I’m using a 25-year forecast period, where ROIC ramps up to 25% by year 15, then gradually declines to 19% 10 years later, such that ROIIC converges with the cost of capital. I actually believe this is conservative. Amazon’s ROIC could eventually go much higher than 25%

Still, this gets me to a fair value of ~$220 using a 10% discount rate. If your hurdle is 12%, you’d want to buy below $158.

ASML

ASML is one of those stocks I now think I pulled the trigger on too early. I got impatient. Don’t misunderstand: it’s a fantastic business and I’m not planning to sell, but I probably wasn’t strict enough with my buy discipline. Last week, I used my updated ASML model to show how to link ROIC into a DCF.

I used a 20-year forecast period, which I think is appropriate given ASML’s characteristics. Its ROIC sits around 60% today and gradually declines to 27.5% by year 20, bringing ROIIC down to 10%. For revenue, I assume ASML reaches €52 billion by 2030, in line with management guidance, and then growth slows to 2.5% over time.

With a 10% discount rate, the fair value comes out to around €500, while the stock currently trades closer to €600, even after a big drop over the past year. So either my forecast period is too conservative, or ASML is still trading at a premium.

That said, I’m not eager to sell a high-quality business just because it looks expensive. And when I reverse-engineer the valuation, the implied discount rate is still a respectable 9%.

Basic-Fit

The DCF model I built for Basic-Fit after the 2024 results still holds up. You can find it in this post. It’s a bit different than the usual model—I start with profit per club and build up to free cash flow from there.

And while the model uses a 20-year forecast period, I assume club growth to stagnate after just 10 years. That makes the model pretty conservative. Given Basic-Fit’s smaller size and more leveraged capital structure, one would also demand a higher required return.

At a 12% discount rate, fair value lies around €38 per share. At 15%, it drops to just under €22. With the stock trading around €18, I still think Basic-Fit offers a solid opportunity—despite the negative sentiment surrounding it.

Summing up today’s price targets: I believe Airbnb and Amazon are both undervalued. Not by a huge margin—they’re not obvious buys—but they do trade below what I think they’re worth. ASML still looks expensive. It’s not wildly overvalued, but I’m not adding at current levels. Basic-Fit, on the other hand, appears significantly undervalued, though I’m staying cautious given the risks involved.

These are my personal price targets based on my own DCF models. That doesn’t mean you should copy them. Always do your own research and adjust for your own assumptions.

Part two will cover my own price targets for the other stocks I own. Going forward, I’ll include price targets in every stock write-up I publish.

In case you missed it:

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.