Uber ($UBER): The Thesis Is Getting Better, The Stock Is Getting Cheaper

Uber Q1 2026 earnings update

An important piece of the Uber thesis comes down to one question: will AVs disrupt Uber or strengthen it? I spent a good amount of time attempting to answer this question in my January deep dive, and my verdict leaned toward the latter: AVs will strengthen Uber’s business.

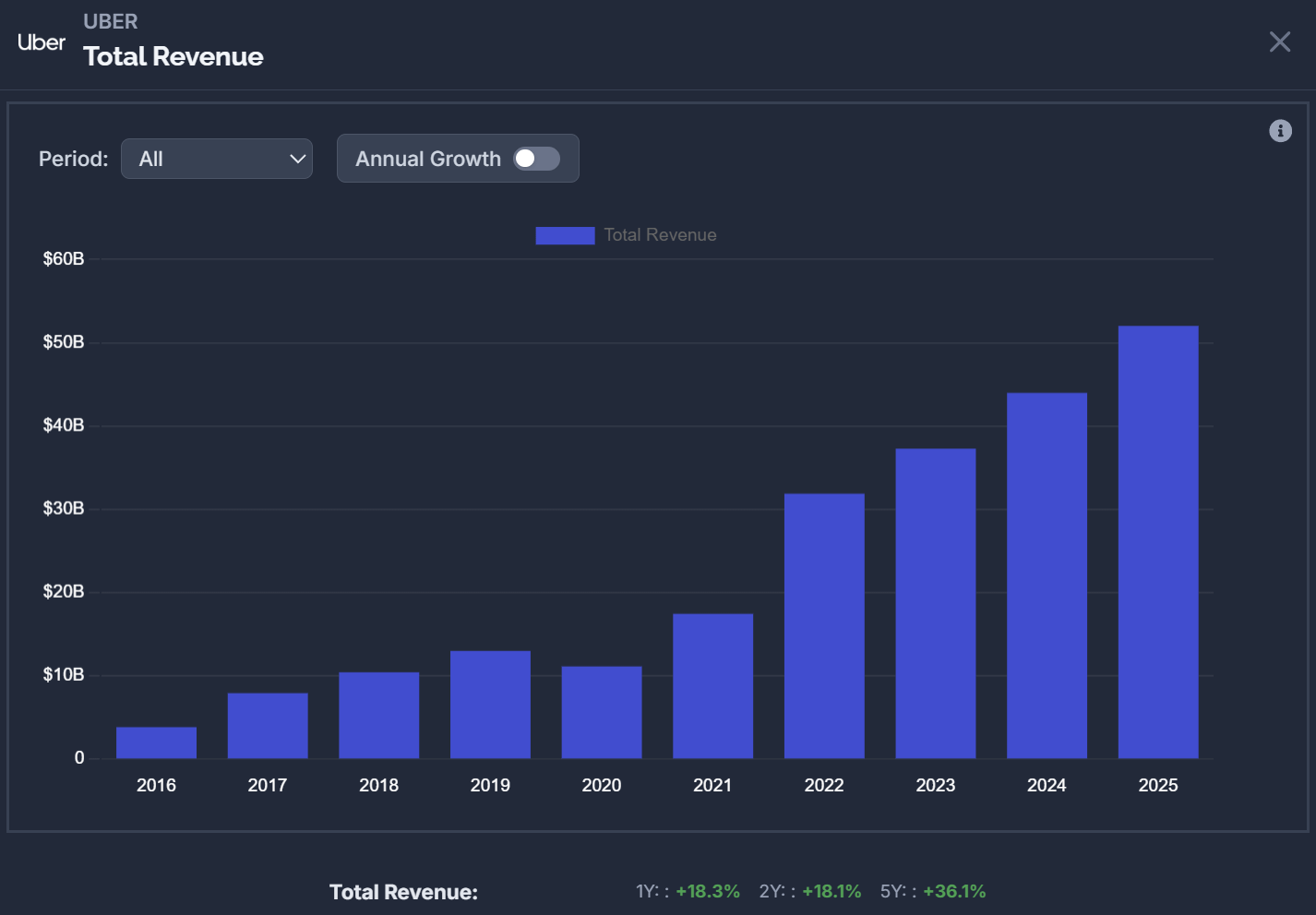

Uber today is the largest ride-hailing platform in the world, newly and decisively profitable (only since 2022), with delivery, advertising, and a fast-growing subscription business stacked on top of it.

Yet I ultimately chose not to invest in Uber because of valuation concerns. At the time, Uber’s TTM FCF, adjusted for stock-based compensation and accrued insurance reserves (more on that later), was $4.1 billion, and shares traded around $85.

The stock price required me to underwrite roughly 20% annual free cash flow growth for a decade, with an adjusted P/FCF multiple of 43x. In other words, a high-quality business, but not at the right price.

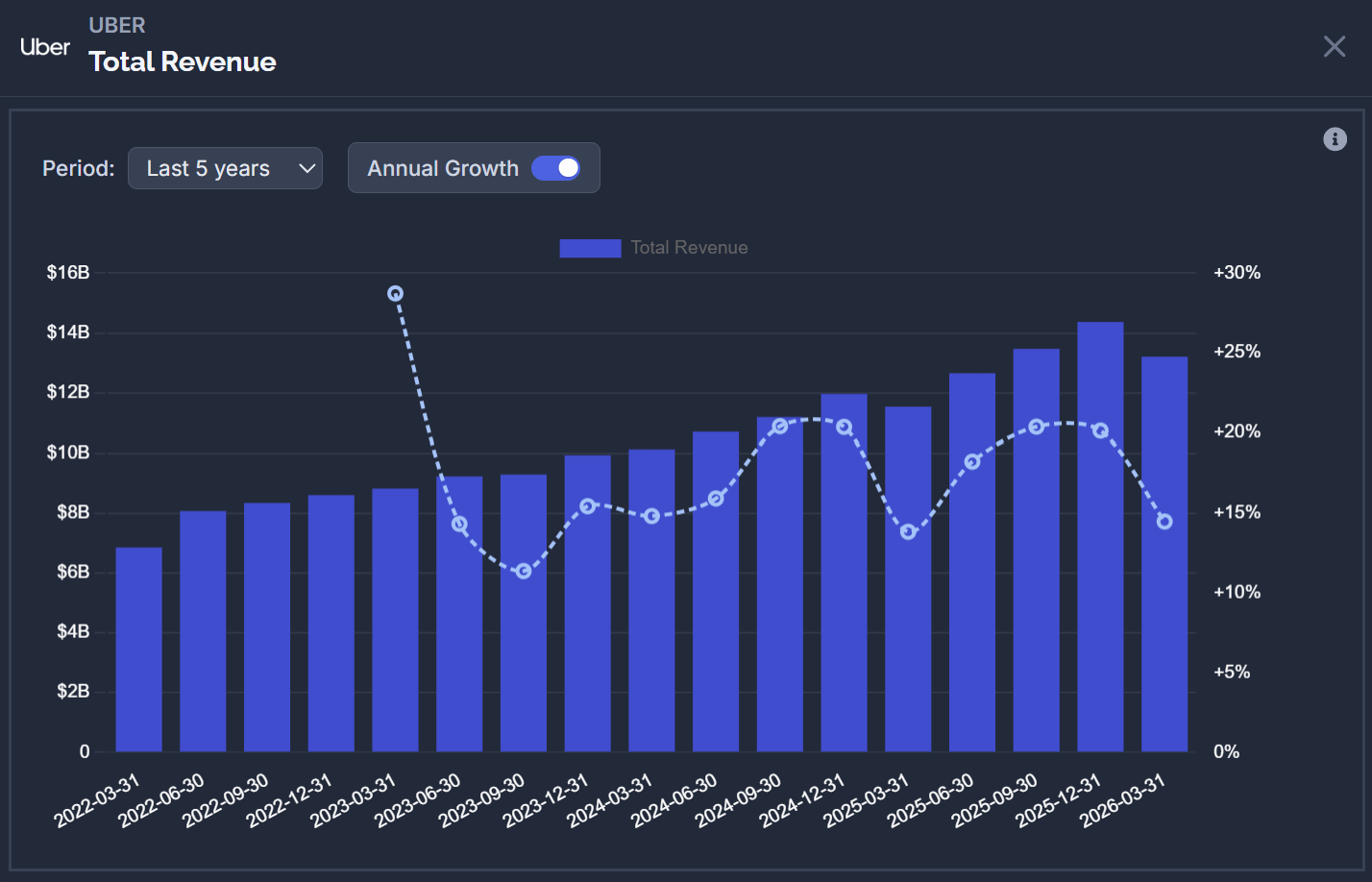

Today, Uber’s TTM FCF has risen dramatically while shares have declined, prompting me to revisit the business and reconsider an investment.

Over the past two quarters, the data on AVs, combined with valuable management commentary, increasingly suggests that AVs are strengthening the business rather than disrupting it.

Two quarters and a roughly 15% lower share price later, it is worth asking what has changed.

The Q4’25 and Q1’26 Numbers

On the surface, both quarters were simply strong.

Q4 2025 trips increased 22% YoY to 3.8 billion, gross bookings of $54.1 billion (also up 22%), and revenue up 20% to $14.4 billion.

For full year 2025, Uber reached $193.5 billion in bookings, up 19% YoY, and $52 billion in revenue, up 18% YoY.

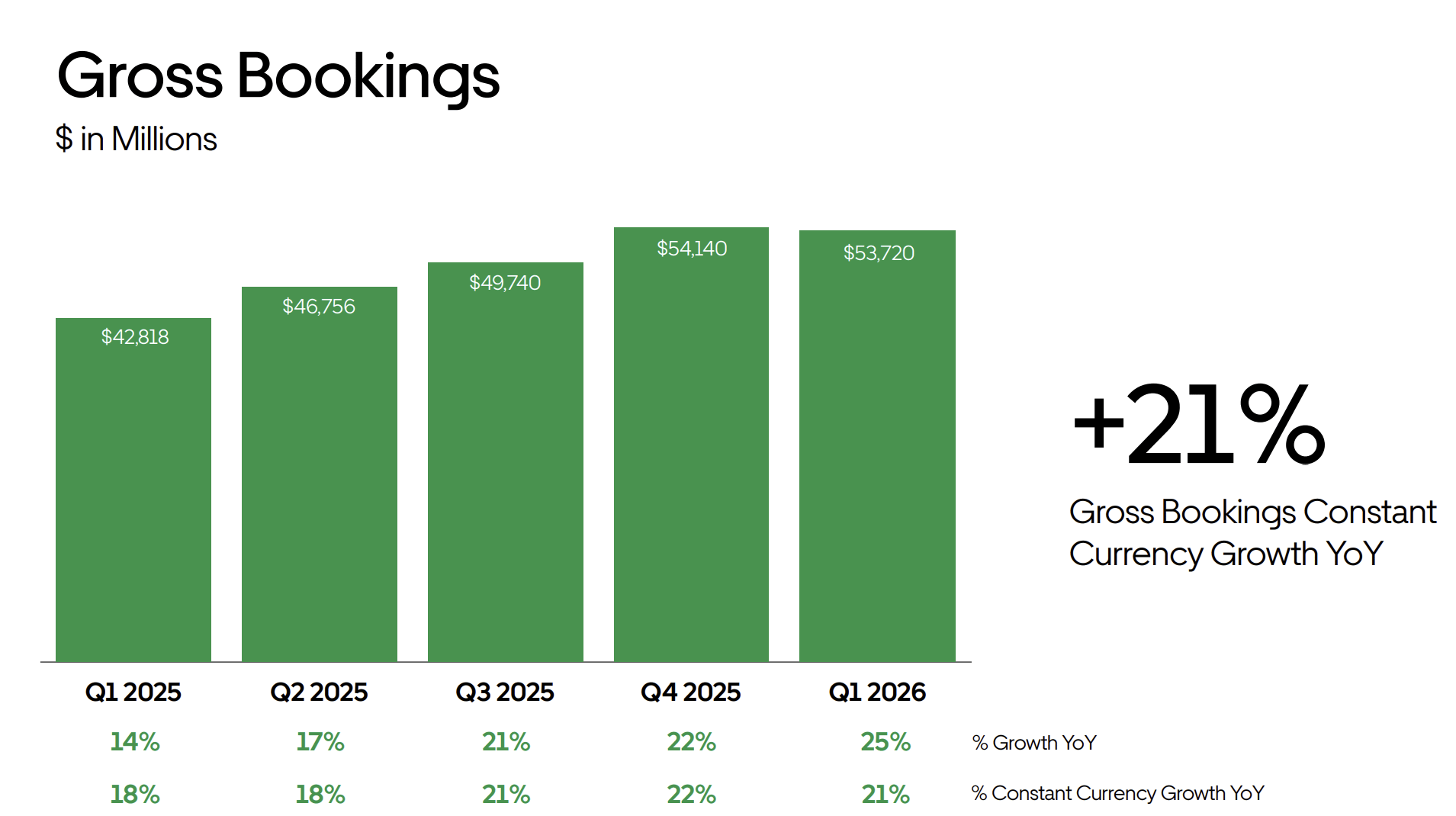

So far, 2026 has been a year of acceleration. Gross bookings in Q1 reached $53.7 billion, up 25%, or 21% in constant currency. Mobility accelerated to 20% growth, Delivery grew 23%, and Freight returning to growth (6% YoY) for the first time in nearly two years.

This acceleration comes as market conditions for auto insurance have improved, allowing Uber to reduce prices and stimulate demand.

“All in all, it's putting us in a place where this will be the first year since COVID where we expect to see good leverage on our insurance cost line for the U.S. Mobility business… As a result of that, we are seeing really good elasticity. And as we would have expected, we've seen that price reduction translate to acceleration in trip growth.”

—Uber CFO Balaji Krishnamurthy

Other growth opportunities as discussed in my original deep dive are also contributing more meaningfully. Uber One membership surpassed 50 million members, growing an exceptional 50% YoY, while trip growth in sparse markets is now growing twice as fast as in core urban markets.

Uber expects its U.S. Mobility business to continue accelerating throughout 2026, while Delivery has already been accelerating for years:

5% bookings growth in Q1 2022

12% in Q1’23

13% in Q1’24

15% in Q1’25

23% in Q1’26

This acceleration has been driven by strong customer retention, membership growth, and the successful expansion of Grocery & Retail (G&R).

“This business [G&R] continues to grow significantly faster than restaurant delivery, driven by increased selection, product innovation, and rising consumer awareness.”

—Uber CEO Dara Khosrowshahi

In Q1 2026, revenue grew just 14%, or 10% in constant currency, versus gross bookings growth of 25%. However, revenue was negatively impacted by a $1 billion accounting headwind related to a business model change in the U.K., equivalent to roughly eight percentage points of growth. Nothing fundamental changed. Revenue growth would have been broadly in line with bookings growth absent this accounting adjustment.

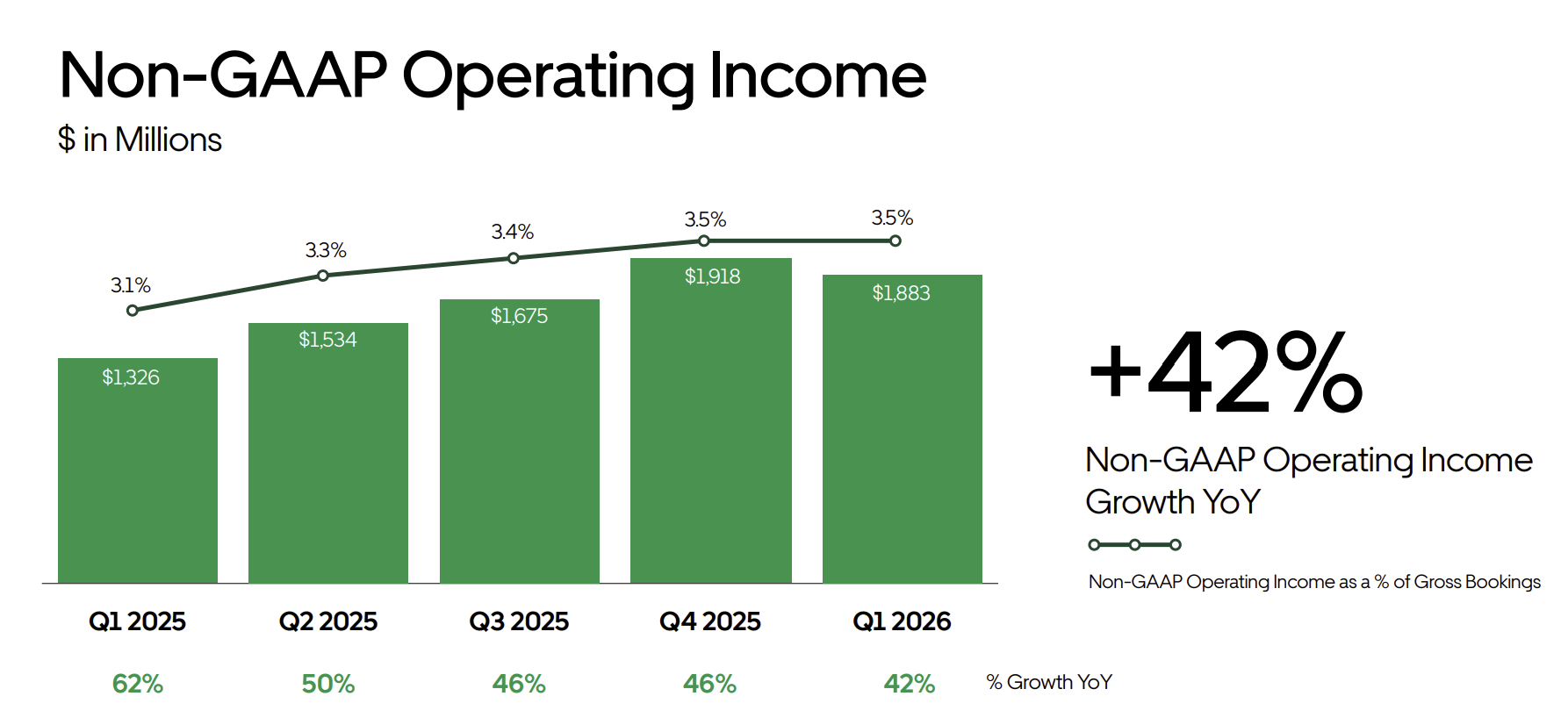

Profitability also continues to improve rapidly. Mobility operating income reached $2 billion, with a record operating margin of 7.7% (defined as operating income divided by gross bookings), while Delivery generated $961 million of operating income and a record margin of 3.7%. Total operating income reached $1.9 billion, with a margin of 3.5%, growing 42% YoY.

At the time of my original thesis, adjusted TTM FCF was $4.1 billion. Two quarters later, adjusted TTM FCF stands at $5.5 billion (after adjusting for both stock-based comp and accrued insurance reserves).

That has significant implications for valuation, which I will discuss shortly.

In just two quarters, Uber has become larger, more profitable, and more cash-generative.

The AV Question Is Starting To Answer Itself

When I first covered Uber, AVs seemed the biggest risk to the investment thesis.

If self-driving technology becomes widespread, drivers disappear. And if drivers disappear, Uber loses its role in the ecosystem.

At the time, my argument was largely based on timing. Even if AVs eventually succeed, commercialization would likely take far longer than most investors expect.

While I still believe that, the more important development is that the early evidence increasingly suggests AVs are strengthening Uber rather than weakening it.

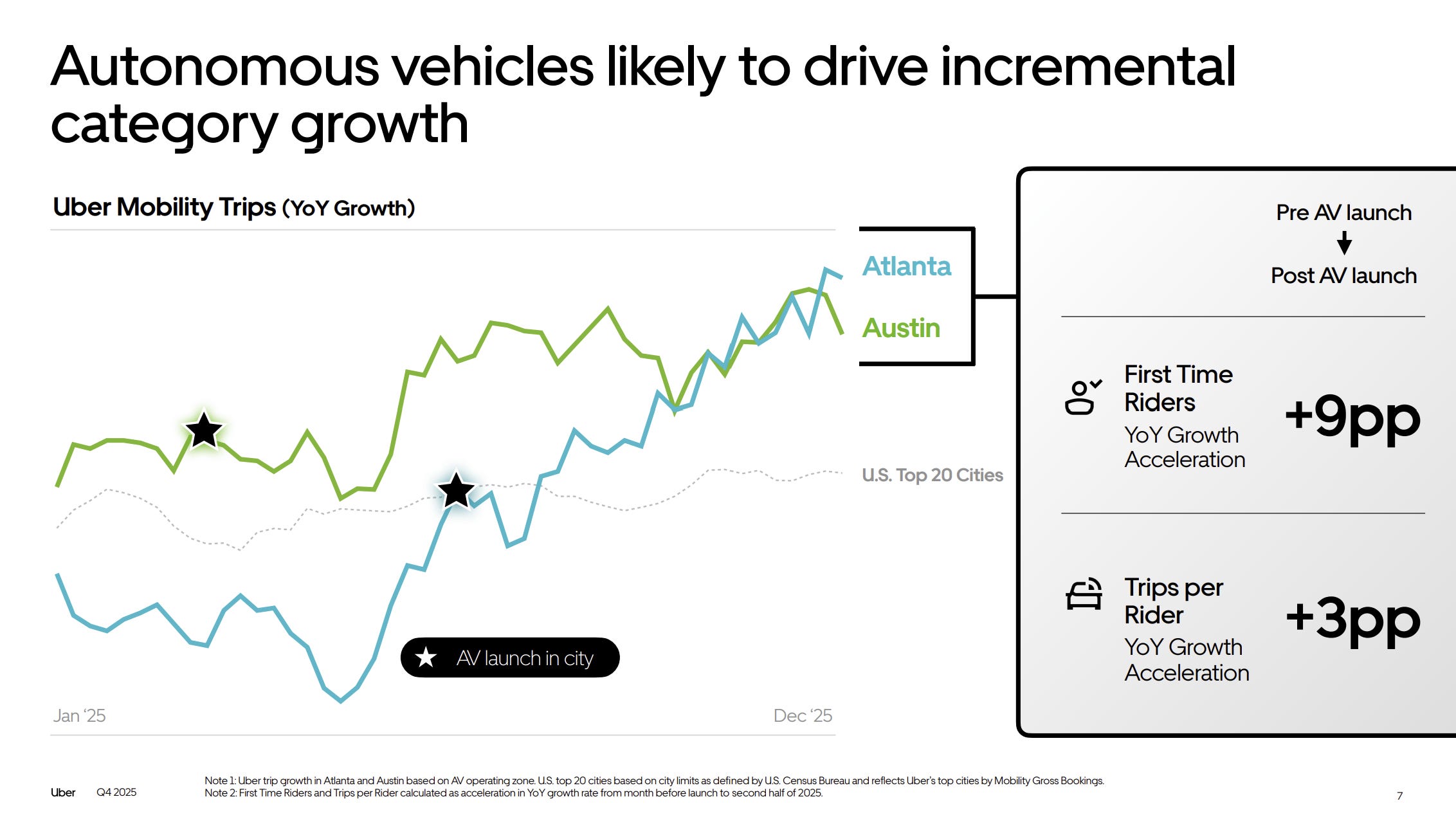

"AVs in the marketplace whether they're competitive in San Francisco or whether they're on our platforms like Austin and Atlanta are turning out to be net positives in growing the overall economic pie."

—Uber CEO Dara Khosrowshahi

The traditional assumption is that AVs simply replace human-driven rides.

Uber believes the opposite. The company is a strong believer in a hybrid-network approach. More supply, enabled by AVs, leads to lower prices, shorter wait times, and greater availability. That attracts new riders and increases ride frequency among existing users.

In Austin and Atlanta, where hundreds of AVs now operate on Uber’s network, overall (AV and non-AV) trip growth accelerated after launch.

“The Austin and Atlanta AV operating zones are now among our fastest-growing areas in the U.S. Encouragingly, the overall growth in these markets was driven by both an acceleration in new riders trying Uber for the first time and higher frequency among existing riders. Importantly, even as AV penetration has grown in both cities, the number of human drivers and their average earnings per hour are both up YoY because of the hybrid-network approach.”

—Uber CEO Dara Khosrowshahi

In other words, AVs are currently expanding the market rather than cannibalizing it.

This makes intuitive sense. Ridesharing is a supply-driven business. The more supply available, the more attractive the platform becomes to riders. Whether that supply comes from human drivers or autonomous vehicles matters very little.

The second worry is that AV operators could simply bypass Uber and operate independently. I already challenged this argument in my original thesis, but it is worth revisiting briefly.

The challenge for standalone AV operators is utilization.

AVs are incredibly expensive assets, and every idle minute is lost revenue. Yet transportation demand fluctuates enormously. A typical Monday generates only about 45% of Saturday demand, while daily troughs can fall to just 5% of peak demand. Managing this variability is difficult.

This is where Uber’s hybrid network becomes valuable.

AVs provide a stable base layer of supply, while human drivers absorb demand spikes.

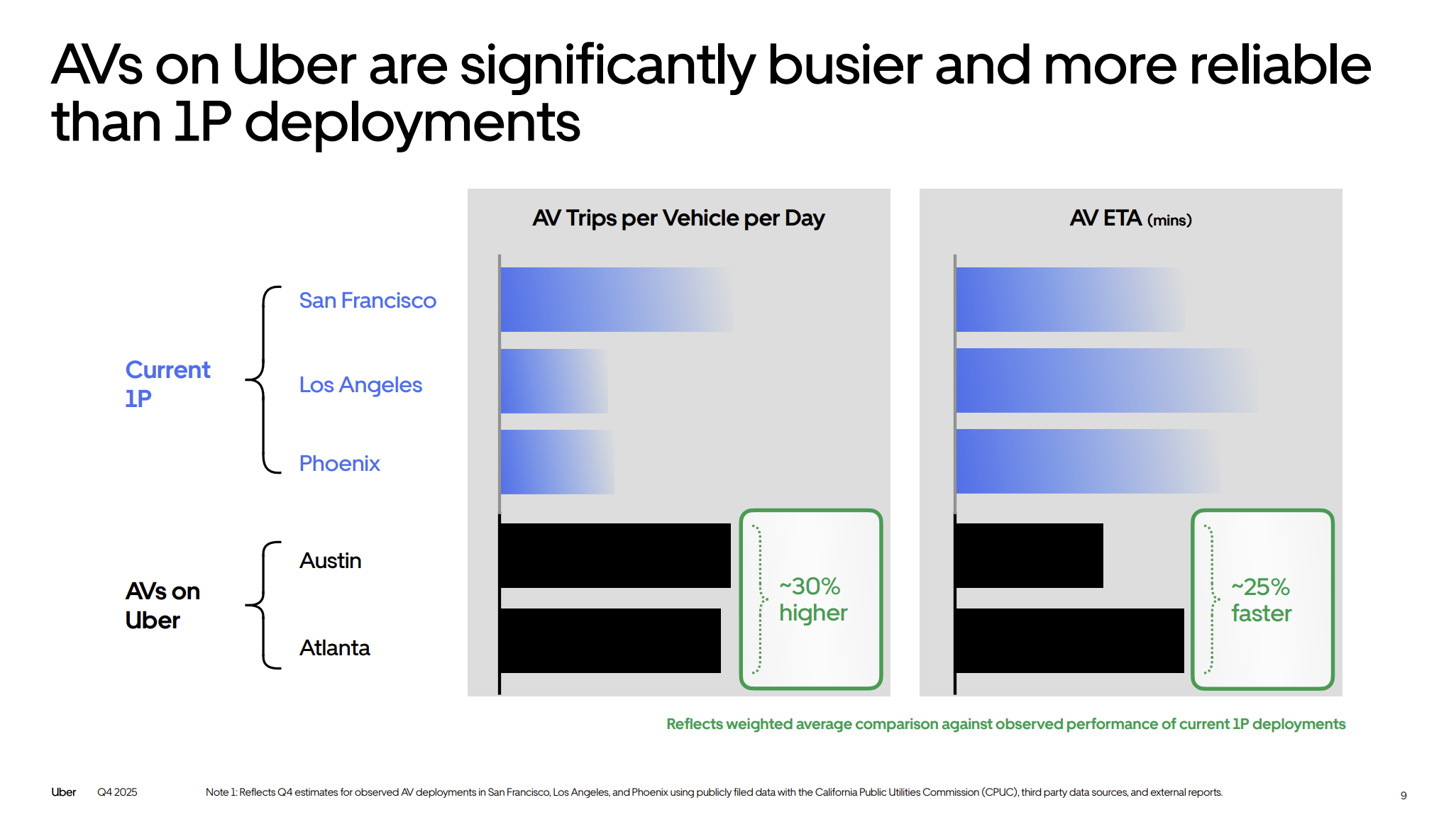

Uber estimates that AVs operating on its marketplace generate about 30% more trips per vehicle per day than standalone AV deployments. Wait times are also roughly 25% faster. Compared with Los Angeles, Uber's hybrid deployments in Austin and Atlanta generate more than twice as many trips per vehicle per day.

"We're seeing AVs on our platform at significantly higher utilization than kind of 1P stand-alone platforms... trips per vehicle per day are 30% higher, ETAs are better as well."

—Uber CEO Dara Khosrowshahi

Uber’s marketplace creates real economic value for AV operators. That is precisely why so many companies are choosing to partner with Uber rather than compete against it.

And despite all the excitement around robotaxis, widespread adoption remains years—even decades—away.

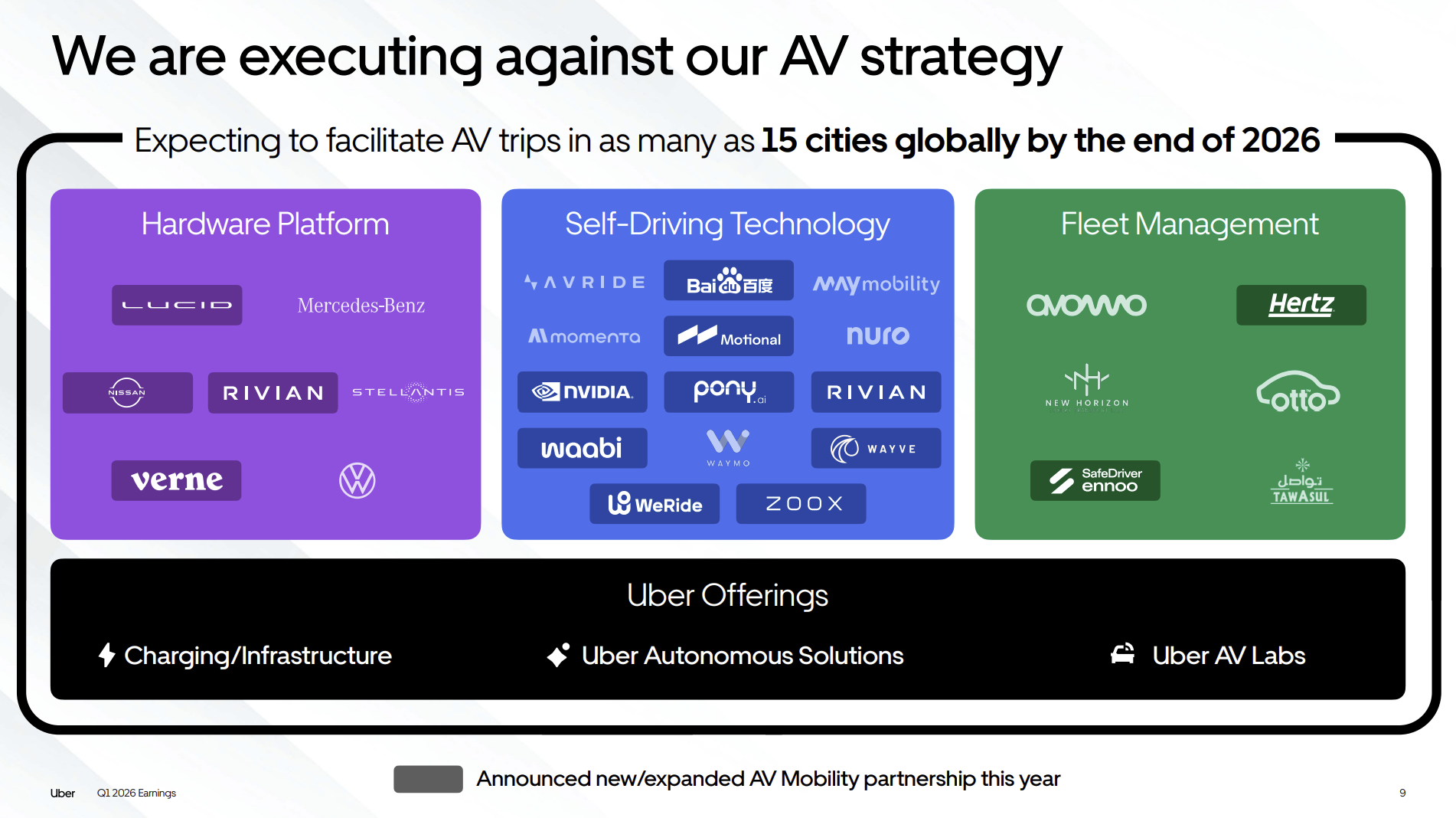

Uber operates in more than 15,000 cities globally and over 8,000 markets in the U.S. Today, Uber is live in 8 cities with AVs, with plans to expand to 15 by year-end.

The list of partners speaks for itself: Wayve, Nissan, Motional, NVIDIA, WeRide, Lucid, Nuro, Waymo, Rivian, Zoox, Verne, Pony.ai, Waabi, and many others. Uber now has more than 30 AV partners, and AV trips increased more than 10x YoY in Q1 2026.

This fragmentation across hardware manufacturers, software providers, and fleet operators plays directly into Uber’s hands.

Uber does not need to build the winning AV. It only needs to remain the platform that aggregates demand.

AVs will transform the supply side of transportation, but they do not necessarily change who owns the customer relationship.

And so far, every quarter that passes makes it look increasingly likely that Uber remains the primary demand aggregator regardless of which AV providers ultimately win.

Has Anything Changed?

The core story over the past six months is simple: growth is accelerating, clarity around AV risk has improved, free cash flow has increased, and the stock price has declined.

At the same time, cross-platform penetration, one of the growth pillars discussed in my original thesis, continues working in Uber’s favor as the company adds more services to its ecosystem.

The grocery delivery business continues to grow rapidly. Uber’s barbell strategy is extending its runway. Most recently, the company added hotels through a partnership with Expedia, where Dara Khosrowshahi previously served as CEO.

The vision of Uber becoming a super app is gradually becoming reality.

So, the core thesis remains firmly intact. While things have changed, nothing has changed for the worse.

Valuation

Uber’s stock now trades just above $70, giving the company a market cap of nearly $150 billion.

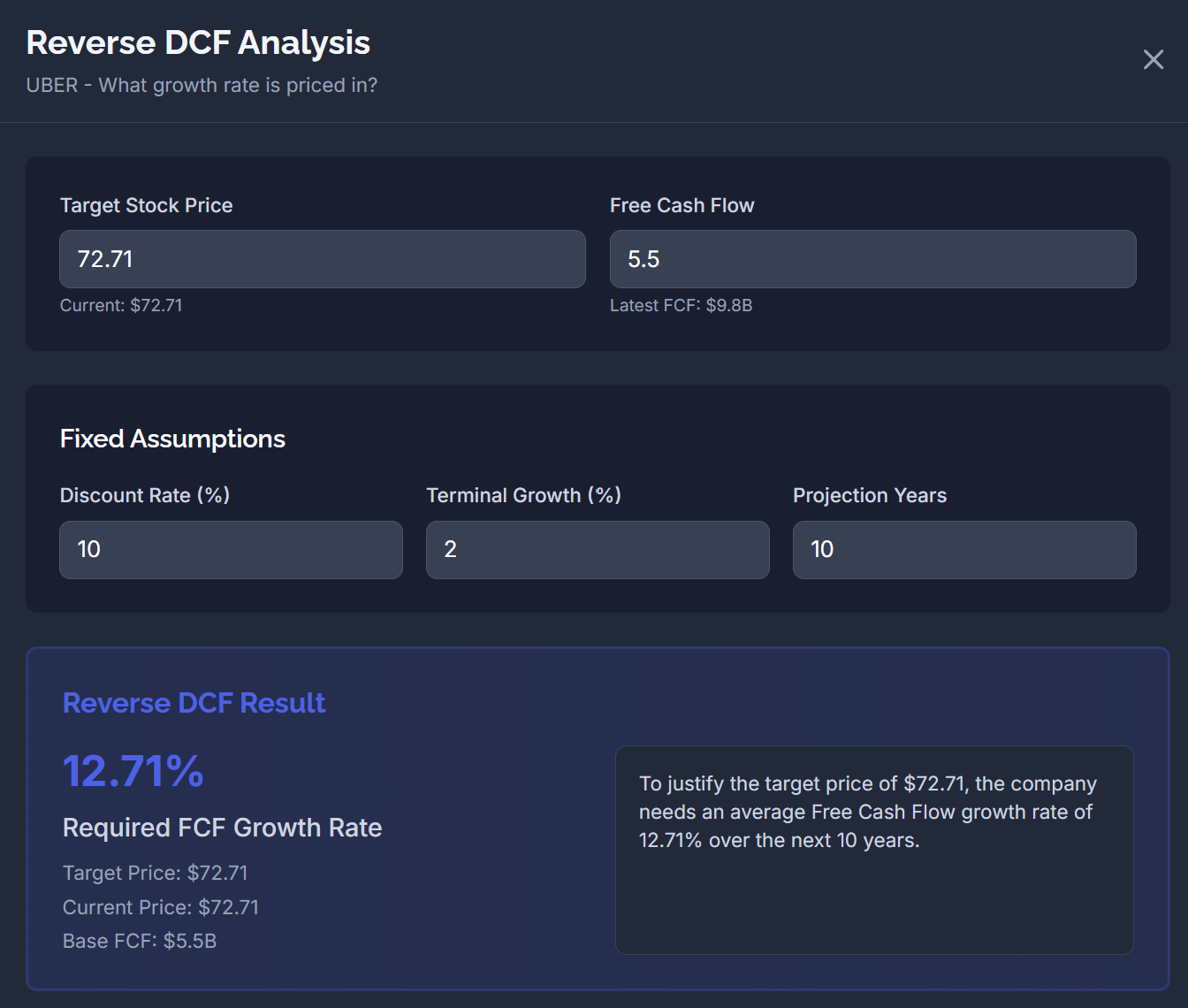

When I researched Uber for my deep dive, shares traded at $85 and adjusted FCF was roughly $4.1 billion, implying an adjusted P/FCF multiple of 43x. My reverse DCF suggested Uber needed to grow FCF by roughly 19% annually to justify the valuation.

Now, unadjusted FCF has reached $9.8 billion, up 42% YoY, while adjusted FCF has reached $5.5 billion, up 34% from the original $4.1 billion base, implying an adjusted P/FCF multiple of 29x, much lower than the initial 43x.

When put together, Uber now requires roughly 13% annual FCF growth to generate a 10% annual return under my reverse DCF assumptions.

Given that stock-based compensation has remained stable, and given that I made a small mistake in my earlier interpretation of accrued insurance reserves, I do not consider that demanding.

The insurance reserve working capital benefit has boosted Uber’s cash flows over the years. Because Uber self-insures part of its auto liability risk, it records insurance expenses when accidents occur but often pays the related claims months or years later. As ride volumes grow, new insurance liabilities are created faster than old claims are settled, causing reserves to increase and boosting operating cash flow.

However, this benefit is not permanent free cash flow. The growing reserve balance is a working capital tailwind. As Uber matures and growth slows, reserves should grow more slowly as well, reducing that benefit over time.

For that reason, I (still) believe it is more conservative to exclude the impact of reserve growth when estimating Uber’s normalized free cash flow.

But in my previous interpretation, I wrote that “today’s inflows will eventually become outflows.” But that is not quite correct. Today’s inflows will at some point disappear, but they should not fully reverse.

Long story short, even after excluding insurance reserve growth, Uber’s valuation looks attractive relative to its current growth profile.

I am considering adding Uber to the portfolio at a price around $70 or lower, starting with a small position. I will notify paid subscribers if I do.

Until next time,

Lucas

Summit Stocks

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

The piece makes a strong case that AVs strengthen the marketplace because supply constraints ease and pricing drops attract more riders. Fair enough. But the durability question is whether Uber keeps extracting the same take rate as AV penetration rises. The article assumes that hybrid network advantage translates into permanent pricing leverage. What I would want to see is whether take rates actually hold up once AV operators have enough scale to negotiate harder—or whether the platform's bargaining power erodes as those operators become bigger, more sophisticated, and less dependent on Uber's network to hit their own utilization targets. The economics work great for Uber today; the open part is whether that math survives when AV operators are no longer desperate for distribution.