This Is Amazon's Playbook

Amazon ($AMZN): Q4 2025 results and valuation

Great investments are typically businesses that can reinvest huge amounts at high returns, and Amazon has historically been a prime example.

Clearly, Amazon is not slowing down. Rather, the company is accelerating at an almost absurd scale. After investing $132 billion in 2025, the goal is now to invest another $200 billion in 2026. And that’s just early guidance: Amazon initially targeted $100 billion capex in 2025 and ended up at $132 billion.

There is a degree of uncertainty around the returns these investments will yield, which is why the stock dipped post-earnings.

I trust Amazon’s management to allocate capital in a disciplined and rational manner. They won’t splash away $200 billion for the sake of it; they see a huge opportunity.

And based on the data we have so far, it’s hard to argue with management, despite analyst and market skepticism and talk of an AI bubble.

For Q4, Amazon reported $213.4 billion in revenue, up 14% YoY, at the top end of guidance ($206 to $213 billion). Operating income also reached the high end of guidance: $25 billion versus $21 to $26 billion.

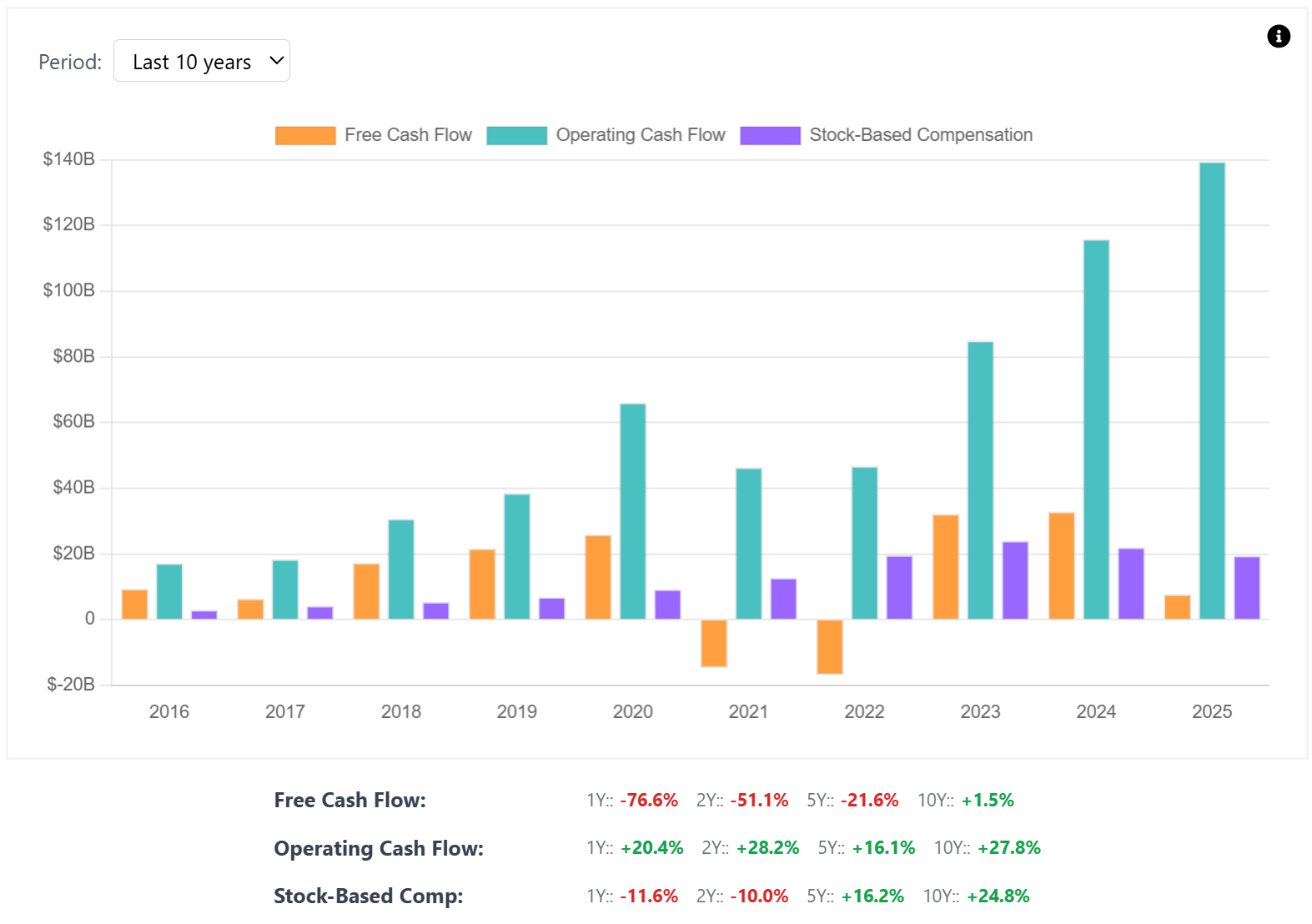

Despite strong results, 2025 free cash flow is now only $11.2 billion, dwarfed by the $132 billion in capex.

Management sees high-return opportunities across many of its businesses: AI, chips, robotics, satellites, quick commerce, and more.

Fueling this ambition for reinvestment is, of course, the cash cow AWS. The segment’s revenue reaccelerated again QoQ, growing 24% YoY to $35.6 billion (20% in Q3 and 17% in Q2). This is the fastest growth in over three years, and AWS is now a $142 billion ARR business.

CEO Andy Jassy once again reminded investors how impressive this really is:

“As a reminder, it’s very different having 24% YoY growth on a $142 billion annualized run rate than to have a higher percentage growth on a meaningfully smaller base, which is the case with our competitors. We continue to add more incremental revenue and capacity than others, and extend our leadership position.”

This growth validates Amazon’s enormous capex plans, as well as the AWS backlog, now at $244 billion, up 40% YoY and 22% QoQ. This is real, tangible validation that the capex story isn’t as uncertain as some think.

This is because capex is once again predominantly going toward AWS. Demand is visible, and capacity is monetized as fast as it is installed.

“We have deep experience understanding demand signals in the AWS business and then turning that capacity into strong return on invested capital. We are confident this will be the case here as well.”

—CEO Andy Jassy

But Amazon isn’t all AWS. North America revenue grew 10% YoY to $127.1 billion, while operating income reached $11.5 billion. International revenue increased 17%, or 11% excluding foreign exchange, to $50.7 billion, with only $1 billion in operating income. AWS operating income was $12.5 billion.

In retail and logistics, Amazon’s competitive advantages are obvious. The company was named the lowest-priced retailer for nine straight years (14% lower), same-day delivery is up 70% YoY, and Amazon Now, ultra-fast delivery within half an hour, is expanding rapidly.

Amazon Ads sits on top of this retail stack as well as Prime Video, and it reached $21.3 billion in revenue, up 22% YoY.

One of Amazon’s younger bets is Amazon Leo, previously known as Project Kuiper. Commercial launch remains planned for 2026, with dozens of commercial agreements already signed.

Amazon has already launched 180 satellites, with another 20 planned for 2026.

The downside of Amazon Leo is that it will pressure profitability in 2026, with about $1 billion in incremental Leo costs expected in Q1 2026, plus International price investments and higher D&A.

Amazon expects revenue of $173.5 to $178.5 billion in Q1 2026, implying very solid growth of 11-15% YoY. The company further expects operating income of $16.5 to $21.5 billion, compared to $18.4 billion in Q1 2025.

Profit and free cash flow growth will remain under pressure in the coming year because of the huge investments Amazon is planning. This is Amazon’s playbook, so I don’t consider this a problem.

Once capex normalizes (though if it’s up to Amazon, they’ll keep reinvesting forever) we should see operating leverage. Employee count growth continues to stagnate, with 1.58 million employees at the end of the quarter, compared to 1.53 million in 2023 and 1.56 million in 2024.

This supports the long-term robotics narrative I outlined in an earlier post.

AI won’t just power robotics, but AWS in particular as well. Management emphasized that real AI adoption forces businesses to migrate to the cloud:

“If you really want to use AI, in an expansive way, you need your data in the cloud and you need your application in the cloud. Those are all big tailwinds pushing people towards the cloud.”

Rufus, Amazon’s AI shopping assistant, is also off to a strong start in 2025. Rufus is already driving conversion and incremental revenue, with 300 million customers using it, and those who use the assistant being 60% more likely to complete a purchase.

Finally, while free cash flow has come down again to just $11.2 billion, operating cash flow increased 20% YoY to $139.5 billion.

At the same time, stock-based compensation continues to decline, now at $19.5 billion.

All in all, this was another strong quarter from Amazon, and with continued double-digit growth, the law of large numbers doesn’t apply to Amazon just yet.

I think the uncertainty around the $200 billion investment plan is mostly overblown. It’s obviously a huge number that makes investors nervous, but there is clear proof this is a rational decision that should result in high returns.

Today, Amazon trades at a P/OCF of 16 times. The question is whether that’s low enough to make Amazon a buy.