Salesforce vs. the SaaSpocalypse

Salesforce Q4 2026 earnings update

The so-called SaaSpocalypse, or whatever you want to call it, is in full swing, and Salesforce remains a big part of it.

Shares are down nearly 50% from their all-time high, and sentiment is low. When Salesforce reported Q4 fiscal 2026 earnings this week, management responded by announcing a huge $50 billion share buyback program and by saying the company will survive this SaaSpocalypse.

Beyond the general SaaS sell-off, Salesforce has struggled with relatively weak organic growth. The question now is whether AI, specifically Agentforce, will genuinely reaccelerate organic growth, or whether growth remains structurally lower.

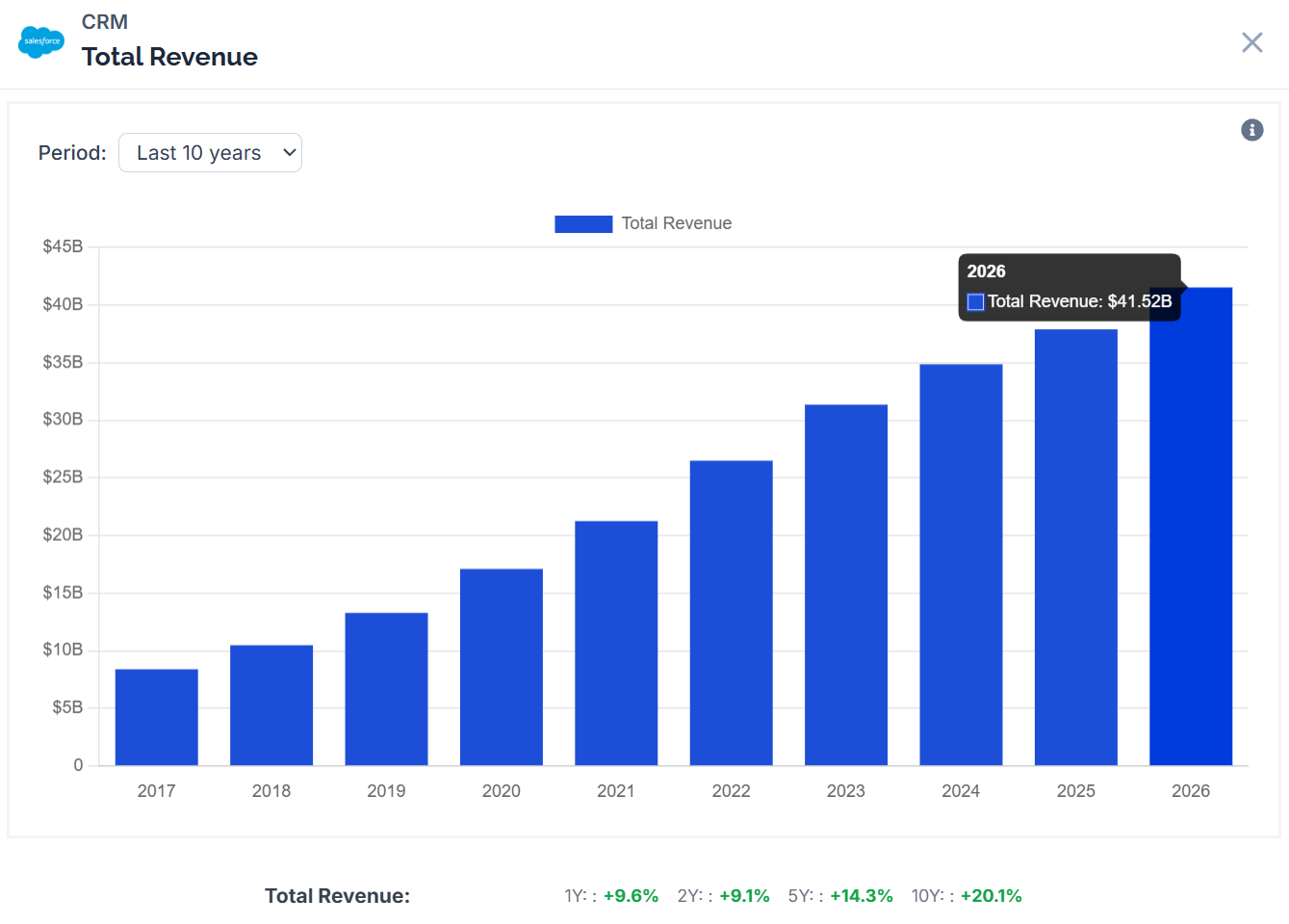

Looking at the headline numbers for Q4 fiscal 2026, results were solid, although the Informatica acquisition contributed:

Revenue grew 12% YoY to $11.2 billion, within guidance of $11.13–$11.23 billion, including a $399 million Informatica contribution.

Full-year revenue reached $41.5 billion, up 10% YoY.

cRPO increased 16% to $35.1 billion, with 4 percentage points from Informatica.

Free cash flow reached $14.4 billion for the full year, up 16% YoY, or $10.9 billion excluding stock-based compensation.

The medium-term revenue target of $60 billion by fiscal 2030 has been raised to $63 billion. Management also guides for fiscal 2027 revenue of $45.8–$46.2 billion, implying growth of 10–11%.

With the updated 2030 target, this implies roughly 11% annual growth in fiscal 2028 and 2029, which is an acceleration compared to 2026, especially in absolute dollar terms.

Management is confident that revenue will reaccelerate in the second half of this year, driven by stronger net new annualized order value, or AOV, momentum.

So far, Salesforce appears able to implement and monetize AI rather than be disrupted by it.

Interestingly, Nvidia CEO Jensen Huang shared his thoughts on the SaaSpocalypse and agentic AI two days ago in a CNBC interview. I think it helps to frame the broader industry narrative.

Huang argues that the market misunderstands AI’s impact on software. He explicitly said he believes the market is wrong. Agents will not replace SaaS tools; they will use them.

SaaS platforms like Salesforce are systems of record. They store the underlying data that AI agents need to function: customer accounts, contracts, workflows, order data, invoices, ad engagement, and much, much more.

AI agents can be powerful, but they need a place to pull data from, write results back into, trigger workflows, and maintain compliance.

Huang provided a simple but great analogy. When we eventually have robots at home, they will not invent their own microwaves or screwdrivers. They will use the tools that already exist. The same logic applies to SaaS platforms. Why reinvent the wheel when it’s right in front of you?

In fact, AI agents could increase usage of SaaS platforms, because digital employees can consume more software than humans. Demand may rise rather than fall.

With Agentforce running on top of Salesforce’s system of record, seat expansion should increase, AI credit consumption should rise, and the platform should not be disintermediated.

Suddenly, AI is not an existential threat, as the market suggests, but a demand amplifier.

You can view the full interview here if you’re interested:

Early evidence appears in the numbers. Agentforce ARR is now $800 million, up 169% YoY and up from $500 million a quarter ago. There have been 29,000 deals since Agentforce launched in 2024, up 50% QoQ. More than 75% of Salesforce’s top 100 wins included Agentforce, Data 360, or both.

60% of Q4 bookings came from existing customers. This supports Huang’s thesis and highlights Salesforce’s distribution advantage.

Now, like with Adobe, there is also concern that even if Salesforce succeeds in an AI-first world, enterprise headcount could shrink. Because Salesforce largely operates on a seat-based model, fewer employees would reduce revenue.

Management provided some context around monetizing AI. First, AI will not necessarily reduce seats, as Huang noted. Agents can also fill seats.

Salesforce monetizes AI in three main ways. It upgrades its 100 million seat installed base to higher-tier subscriptions with embedded AI and Agentforce, driving higher ARPU. It expands seat count as improved ROI allows customers to roll out Salesforce to more employees. And it sells consumption-based credits, meaning the more AI is used, the more Salesforce earns.

It is becoming clearer that the SaaS sell-off is unjustified. I discussed this implicitly in my recent Adobe update, but there is little evidence that the worst fears are materializing.

That suggests Salesforce and other SaaS stocks could be great opportunities today.

Salesforce generated $10.9 billion in free cash flow excluding stock-based compensation for the full year. With $5.6 billion in net cash, the company trades at an EV/FCF of 16x.

To justify today’s price, Salesforce would need to grow free cash flow at less than 6% annually, assuming a 10% discount rate and 2% terminal growth rate.

Market expectations are very undemanding.

Management agrees by announcing the $50 billion share buyback program, as well as by explicitly saying “these are some low prices.” Yes, CEO Marc Benioff is the type of person to exaggerate, but in this case, I don’t think he’s wrong.

There is significant value at today’s price, especially if you do not believe in the SaaSpocalypse, which I do not.

I continue to hold Salesforce and may add shares in the near future. Paid subscribers will be notified.

Thanks for reading.

Lucas

Author & Founder, Summit Stocks

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

It’s wild to see Salesforce pivoting so hard toward Agentforce while trying to shake off that "SaaSpocalypse" label.

Do you think the $50 billion buyback is a genuine sign of confidence in their AI growth, or is it more of a defensive move to keep shareholders happy while organic growth stabilizes?

I’ve subscribed and would be happy to support each other. :)

Jorrit

I think their switching cost moat is substantial enough to hold off AI disruption for a few years, but they definitely need to accelerate their transition to avoid over-relying on subscription revenue.

I just wrote a piece about the keys that SaaS companies need to stay antifragile right now. I think it ties in with your points. If you're interested, I'd love your feedback. Thanks!