Amazon Q4 And Full-Year Earnings

Explosive earnings growth, optimizing retail, and continued capex investments

Today, we’re taking a look at Amazon’s earnings and we’ll reflect on the stock’s valuation.

Amazon is by far my largest holding, and not without reason. It’s been a while since I write my deep dive, but I’m as confident as ever in the company today.

What You’ll Read Today

Full-Year Results

Amazon’s Current Valuation

Full-Year Results

Yesterday, Amazon published its fourth-quarter and full-year 2024 results.

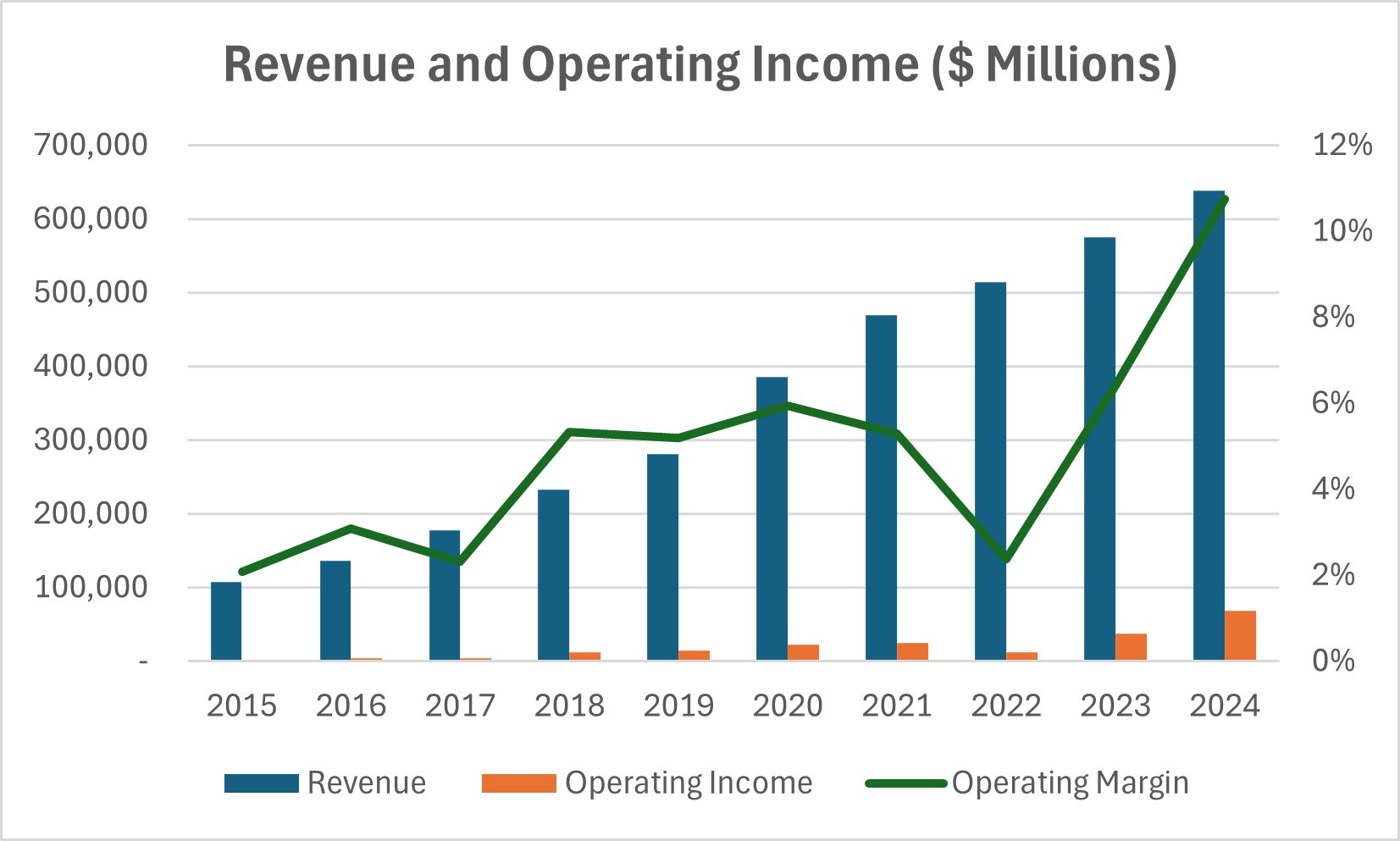

Q4 revenue came in at $187.8 billion, up 10% year-over-year. A stronger dollar created a $700 million greater-than-expected FX headwind, but on a constant currency basis, revenue grew 11%. Operating income grew by 61% to $21.2 billion. For the full year, revenue increased 11% to $638 billion, while operating income soared 86% to $68.6 billion.

CEO Andy Jassy pointed to major efficiency improvements in Amazon’s fulfillment network as a major driver of profitability. Optimized inventory placement, better packaging strategies, and over 60% more same-day delivery sites have reduced per-unit transportation costs while improving speed and selection. Amazon expects further savings as it scales automation and robotics in its logistic operations.

I think this can become a huge driver of profit growth. The retail business is massive, with first- and third-party sales reaching $123 billion this quarter. Even small margin improvements in retail can have an outsized impact on overall profits.

Amazon’s advertising business also continues to expand, with Q4 revenue of $17.3 billion, making this a $69 billion annual revenue run rate business. Jassy highlighted that Amazon has made full-funnel advertising more accessible and effective, allowing businesses to target customers at multiple points—from discovery on Prime Video and homepage placements to more specialized product search ads.

AWS remains key, with Q4 revenue rising 19% to $28.8 billion, reaching a $115 billion annual run rate. Jassy was particularly optimistic about the long-term opportunity:

“AWS is a reasonably large business by most standards, and though we expect growth will be lumpy over the next few years… it's hard to overstate how optimistic we are about what lies ahead for AWS' customers and business.

Amazon signed new AWS agreements with companies like Intuit, PayPal, and Reddit during the quarter.

Beyond AWS, Amazon continues to invest across the business, including in Project Kuiper. One detail that stood out to me was CFO Brian Olsavsky’s reminder that while most Kuiper costs are currently expensed, certain costs will be capitalized once the project reaches commercial viability. A lot of profit is essentially hidden—and not just because of Kuiper—due to Amazon expensing a lot of its investments. In 2024, “Technology and infrastructure” spending—which roughly corresponds to R&D—hit $88.5 billion. Of course, not all of that is pure R&D; some includes depreciation and amortization related to AWS infrastructure. It’s still interesting to think this through.

Amazon’s Q4 capex was $26.3 billion, and 2025 capex is expected to remain at a similar pace—exceeding $100 billion for the year. The vast majority of this will go toward AWS.

“It's the way that AWS business works and the way the cash cycle works is that the faster we grow, the more capex we end up spending… We don't procure it unless we see significant signals of demand. And so, when AWS is expanding its capex, particularly in what we think is one of these once-in-a-lifetime type of business opportunities like AI represents, I think it's actually quite a good sign, medium to long term, for the AWS business.”

For Q1 2025, Amazon projects revenue between $151 billion and $155.5 billion, reflecting 5-9% year-over-year growth. There are some headwinds here, including a $2.1 billion FX impact and a tough comparison to Q1 2024, which had an extra day that contributed around $1.5 billion in revenue. Operating income is projected between $14 billion and $18 billion.

Overall, I think it was a very solid quarter. AWS is still Amazon’s long-term growth engine, but I also like the optimism around margin improvement and efficiencies in retail. Free cash flow in 2025 won’t be high, given the $100 billion planned capex, but I’m completely fine with that.

Amazon’s Current Valuation

Where I first tried to project Amazon’s future free cash flows to assess its valuation, I increasingly realize that it’s a lot more complicated with Amazon than with other companies. Throughout its history, Amazon has never fully optimized for free cash flow generation, and that will not change in 2025. Given the unpredictable nature of its investments, trying to project free cash flow right now feels like pure guesswork, so I’ll refrain from doing that.

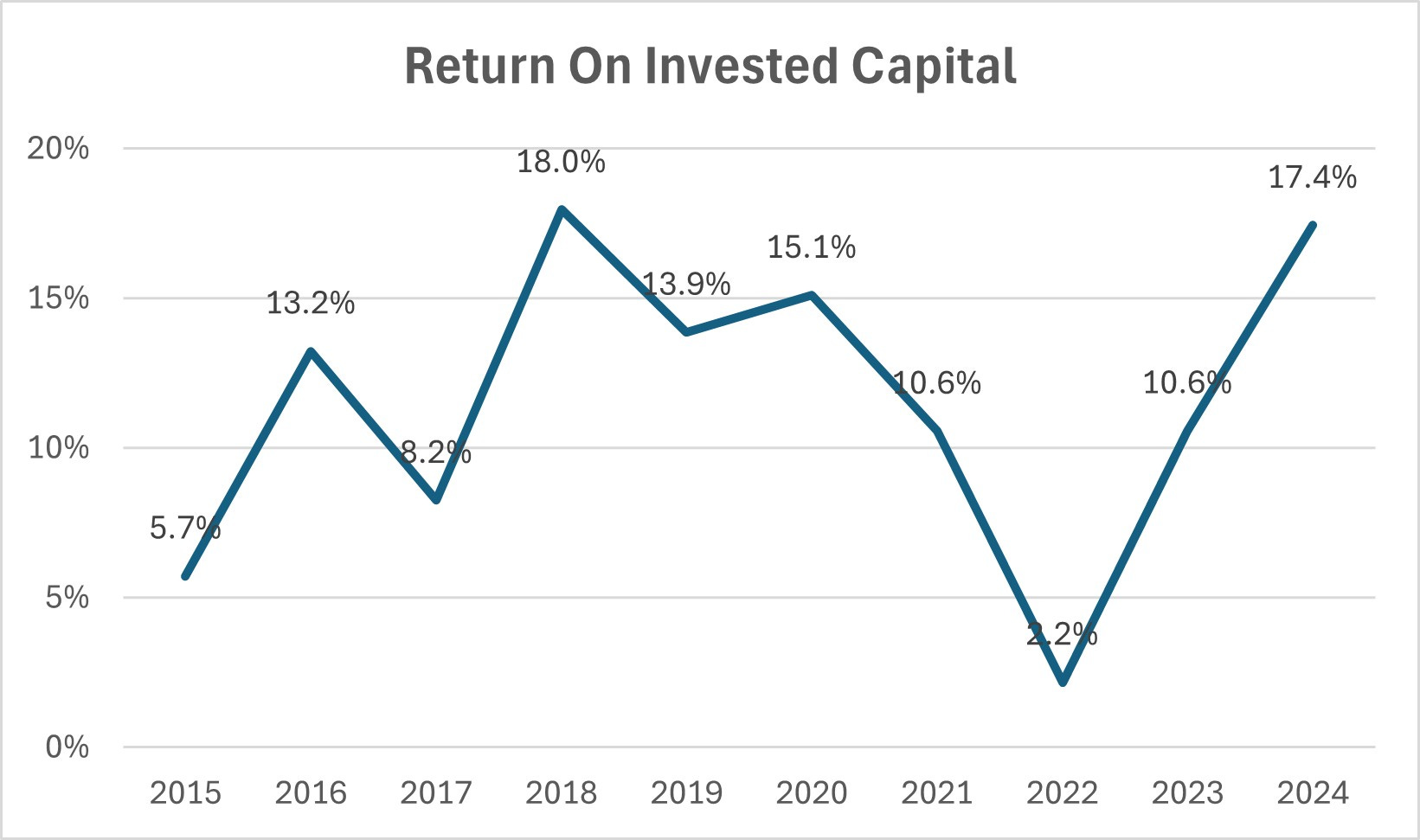

What is clear, however, is that Amazon’s ongoing investments are likely to create significant value for shareholders. In 2024, Amazon’s ROIC reached 17%, up from 10.6% in 2023, and its 1-year incremental ROIC is nearly 80%. With almost $85 billion in capex for 2024 and a projected $100+ billion for 2025, the returns on these investments—if even moderately high—should lead to continued, and potentially explosive, profit growth in the medium term.

I’m confident in Amazon’s direction and happy to continue holding my position, knowing that management is finding strong opportunities to allocate capital effectively. And with operating cash flow excluding stock-based compensation of $94 billion, Amazon doesn’t even look overly expensive. Of course, that’s not a proper way of valuing a stock, but it gives us some indication of where things stand. And as I said earlier, I wouldn’t be surprised if operating cash flow (or operating profit) continues to see significant growth in the coming years.

After Amazon released its earnings, the stock dropped a few percent in after-hours. If negative sentiment takes hold, I might increase my stake, even though it’s already my largest position.

In case you missed it:

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

Beauty of the markets is that we can delegate the capital allocation decisions of our money to the Amazon management.

Good work.