Adobe ($ADBE): The Market Is Missing The Bigger Picture

Adobe Q2 2026 earnings update

Adobe’s thesis still revolves around one central question: will AI disrupt or strengthen Adobe? The market believes in disruption, or at least remains highly uncertain. And uncertainty creates sell-offs.

The data over the past several quarters, however, suggests the complete opposite.

The argument for contrarians like me was never that Adobe would build the best AI models or capture the entire image-generation market. The argument was that Adobe already owned the customer relationship.

With over 850 million MAUs, Adobe possesses one of the strongest distribution moats in software. As AI has become increasingly important, Adobe has been able to distribute those capabilities across its existing customer base rather than watching customers leave for AI-first competitors.

At the same time, Adobe’s other competitive advantages remain strong.

Creative professionals, enterprises, agencies, marketers, and publishers have built entire workflows around Adobe products. Switching costs are enormous. The ecosystem is deeply embedded in creative and business processes.

And despite years of Gen-AI innovation and AI challengers like Canva, Midjourney, OpenAI, Runway, and countless startups, Adobe continues growing revenue by around 10% and its customer base by roughly 20%.

Back in February, I discussed the most important bear cases for Adobe and concluded that none were showing up in the numbers.

Q2 2026 is yet another quarter that reinforces that conclusion.

In fact, the evidence supporting the thesis may be stronger today than when I first invested.

The Q2’26 Numbers

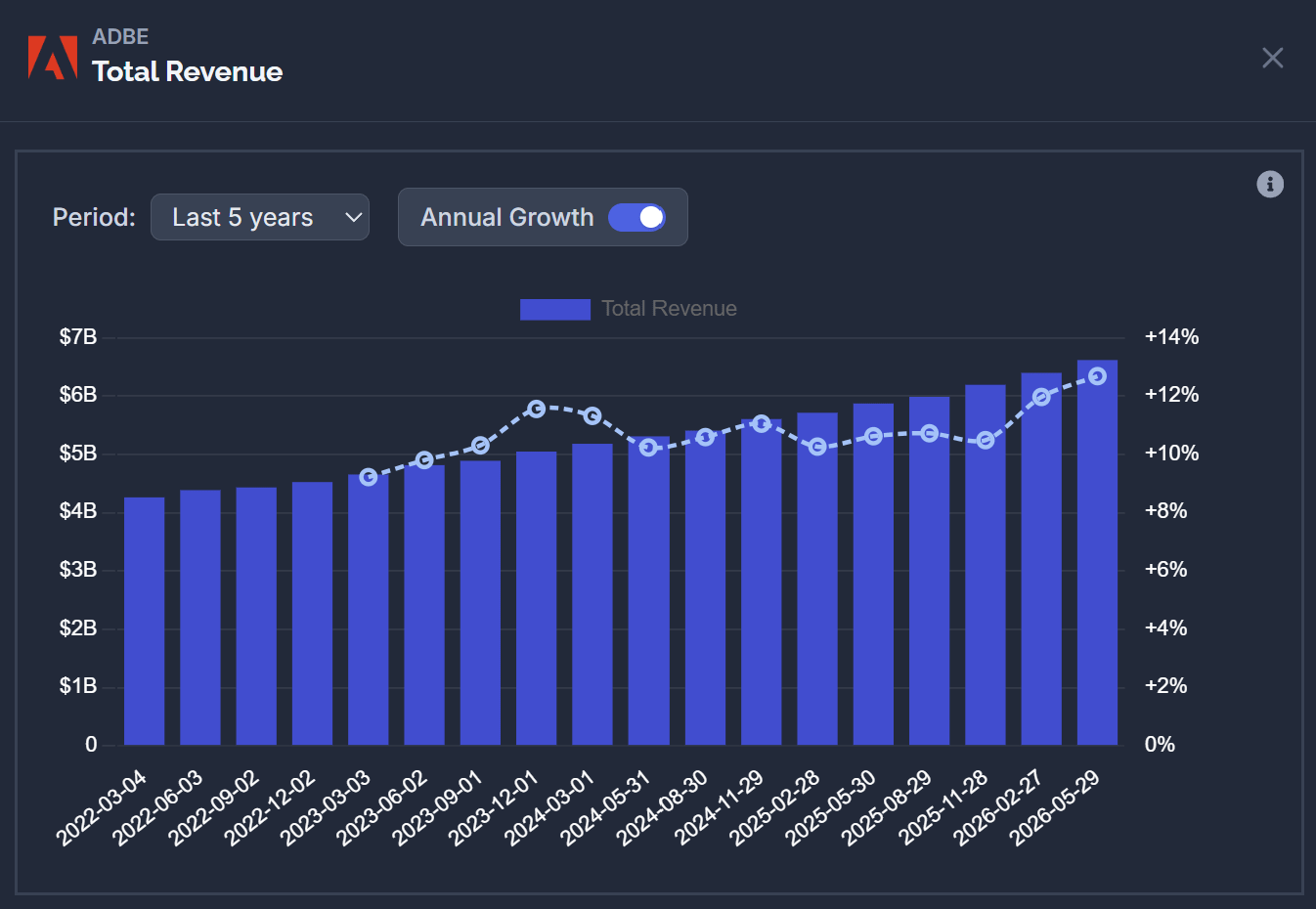

Adobe reported revenue of $6.62 billion in Q2, up 13% YoY and above guidance of $6.43-6.48 billion.

RPO reached $22.3 billion, with both RPO and cRPO growing 13% YoY. In other words, future revenue visibility remains healthy and customers are still signing contracts (as usual).

Subscription revenue remained strong across both major customer segments.

Business Professional & Consumers generated $1.85 billion of subscription revenue, growing 15% YoY. That includes—as it says—consumers, the customer group investors are most concerned about when it comes to potential churn toward AI solutions.

Creative & Marketing Professionals generated $4.54 billion, up 11% YoY.

For Q3, management guided revenue of $6.67-6.72 billion, implying approximately 12% growth.

And Adobe raised full-year guidance.

Management now expects revenue of $26.5-26.6 billion in 2026, compared to prior guidance of $25.9-26.1 billion.

This increase was driven by the SEMrush acquisition, which added $480 million in ARR to Adobe’s business.

Excluding SEMrush, I think guidance would have remained stable or even been slightly lowered, given two deliberate headwinds.

First, Adobe is shifting toward a more freemium-oriented onboarding strategy for products like Firefly and Express. Reducing friction for new users should further accelerate MAU growth and improve long-term customer lifetime value, but it comes at the cost of slower short-term ARR growth.

Second, Adobe has chosen to delay previously planned Creative Cloud price increases in the second half of the year to support customer acquisition through the freemium strategy.

Both decisions create short-term pressure on ARR growth, but both represent deliberate investments in expanding Adobe’s user base and long-term monetization opportunity.

These decisions come as management explained that AI is changing customer behavior. Adobe has traditionally optimized for direct conversion, with users visiting adobe.com and quickly being pushed toward paid subscriptions.

But now, customers increasingly arrive with a specific task in mind. Generate an image, edit a PDF, create a video, etc.

They want immediate results, which is why Adobe is leaning aggressively into freemium onboarding.

Traffic to adobe.com grew an incredible 40% YoY. Here’s David Wadhwani, President of Adobe’s Creativity & Productivity Business, explaining the entire situation:

“The demand for these new AI experiences begins with LLM conversations and intent-based searches and requires immediate gratification, so is best served with friction-free experiences... While we continue to attract strong traffic to adobe.com, which grew over 40% year-over-year, our traditional direct-to-pay journeys may not always fulfill visitor intent... Given products like Adobe Firefly, Express, and Acrobat AI Assistant have friction-free onboarding and significant adoption, we can now rebalance our journeys to better serve this new generation of users rather than send them predominantly to direct-to-paid journeys.”

Creative freemium MAUs increased from 50 million to 90 million YoY, while Acrobat and Express MAUs now exceed 850 million, up from 700 million a year ago.

On the surface, this was simply another strong quarter.

The Distribution Moat Is Becoming More Valuable

A central part of the Adobe thesis is the importance of distribution. Distribution matters more than having the best AI models.

With its vast customer base, Adobe can cross-sell AI features to existing customers. Alongside incremental revenue, this helps retain customers and reduces the incentive to switch to AI-native alternatives.

While management did not provide specific retention figures, it highlighted that enterprise customers with more than $10 million in ARR grew over 20% YoY and that Adobe saw “continued strength in retention across the enterprise customer base.”

This customer cohort also grew more than 20% YoY in Q1.

Adobe’s AI-first ARR now exceeds $500 million, growing more than 3x YoY.

Firefly ARR increased 50% QoQ. While management did not disclose a specific figure, Firefly ARR exceeded $250 million in Q1 2026, suggesting it is now at least $375 million.

The number of generated enterprise assets increased more than 4x YoY. Put differently, AI usage among Adobe’s most important customers is growing rapidly.

Adobe Foundry surpassed 2,500 custom enterprise models in Q1 2026, and Adobe is now partnering with NVIDIA to further upgrade Foundry:

“Our announced NVIDIA partnership will bring accelerated computing to Adobe Firefly Foundry for faster, higher performing custom models across image, video, audio, vector, and 3D plus a cloud-native 3D digital twin built on Omniverse and OpenUSD.”

—David Wadhwani, President Creativity & Productivity Business

Meanwhile, Adobe continues signing some of the largest companies in the world, including SAP, ServiceNow, Coca-Cola, Merck, and Workday.

This is the exact opposite of what AI disruption is supposed to look like.

Instead of enterprises abandoning Adobe in favor of AI-native competitors or in-house AI solutions, enterprises are adopting AI through Adobe.

Adobe is becoming the vehicle through which AI is delivered.

AI Is Expanding The Market

The other bear case is that AI increases productivity so dramatically that fewer creative professionals will be needed.

Fewer professionals would imply fewer seats. And fewer seats would imply lower revenue.

But what if the opposite is happening? What if AI increases content output so much that demand for creation rises faster than productivity?

Several metrics point in that direction:

Adobe Express MAUs grew more than 20% QoQ

Express users inside Acrobat exported 9x more content than a year ago

Generated enterprise assets increased 4x YoY (as mentioned before)

Alongside these figures, management repeatedly emphasized that content creation is exploding:

“Content creation designed specifically for marketing use cases is exploding.”

“Demand for AI content creation is exploding across ideation, generation, and semantic editing, and generative creative consumption continues to show strong growth.”

“These results underscore the continued explosion in content and the imperative to deliver personalized customer experiences at scale.”

This matters for Adobe for three reasons.

First, Adobe wants to retain its customers, and customers getting more value from Adobe’s products helps keep them aboard.

Second, if content output increases, seat counts will not decline, removing a potential headwind.

Third, Adobe’s monetization increasingly includes usage-based components such as generative credits. Prior to AI, higher productivity inside Adobe products did not generate additional revenue. Customers paid the same subscription fee regardless of usage intensity.

Now, higher productivity can directly translate into higher revenue.

The more content customers create, the more opportunities Adobe has to monetize AI.

Has Anything Changed?

The short answer is no. The original thesis appears stronger today than it did a year ago.

The moat remains intact, enterprise adoption remains strong, and AI monetization continues to grow nicely.

The only meaningful change this quarter is that Adobe is becoming more aggressive in how it acquires and monetizes users.

Management is willingly sacrificing some short-term ARR growth to accelerate customer acquisition and build a larger long-term opportunity.

I view that as a positive.

Valuation

While I just said nothing has changed (for the worse), one thing has changed: the stock price.

During my Q1 2026 update in March, shares traded around $250. They now trade just above $200.

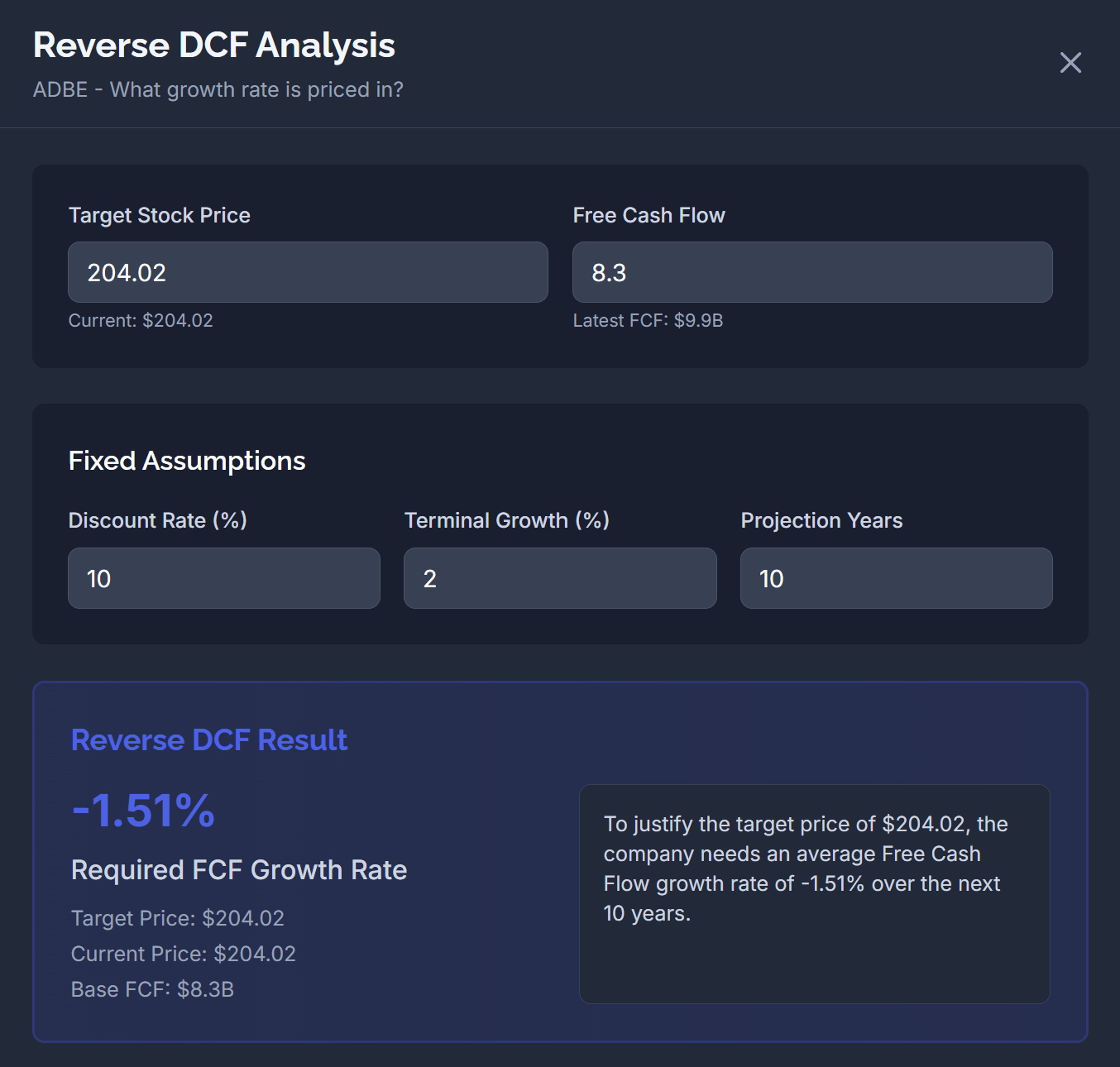

With $10.3 billion in TTM free cash flow, or $8.3 billion when adjusted for stock-based compensation, Adobe now trades at a P/FCF of 8x, or 10x when adjusted for stock-based compensation.

This is an incredibly low valuation.

To put this into perspective, Adobe does not even need to grow its adjusted free cash flow over the next decade to justify the current share price.

Free cash flow can decline by 1.5% annually and investors would still earn a 10% annual return (based on the 10% discount rate used in the reverse DCF).

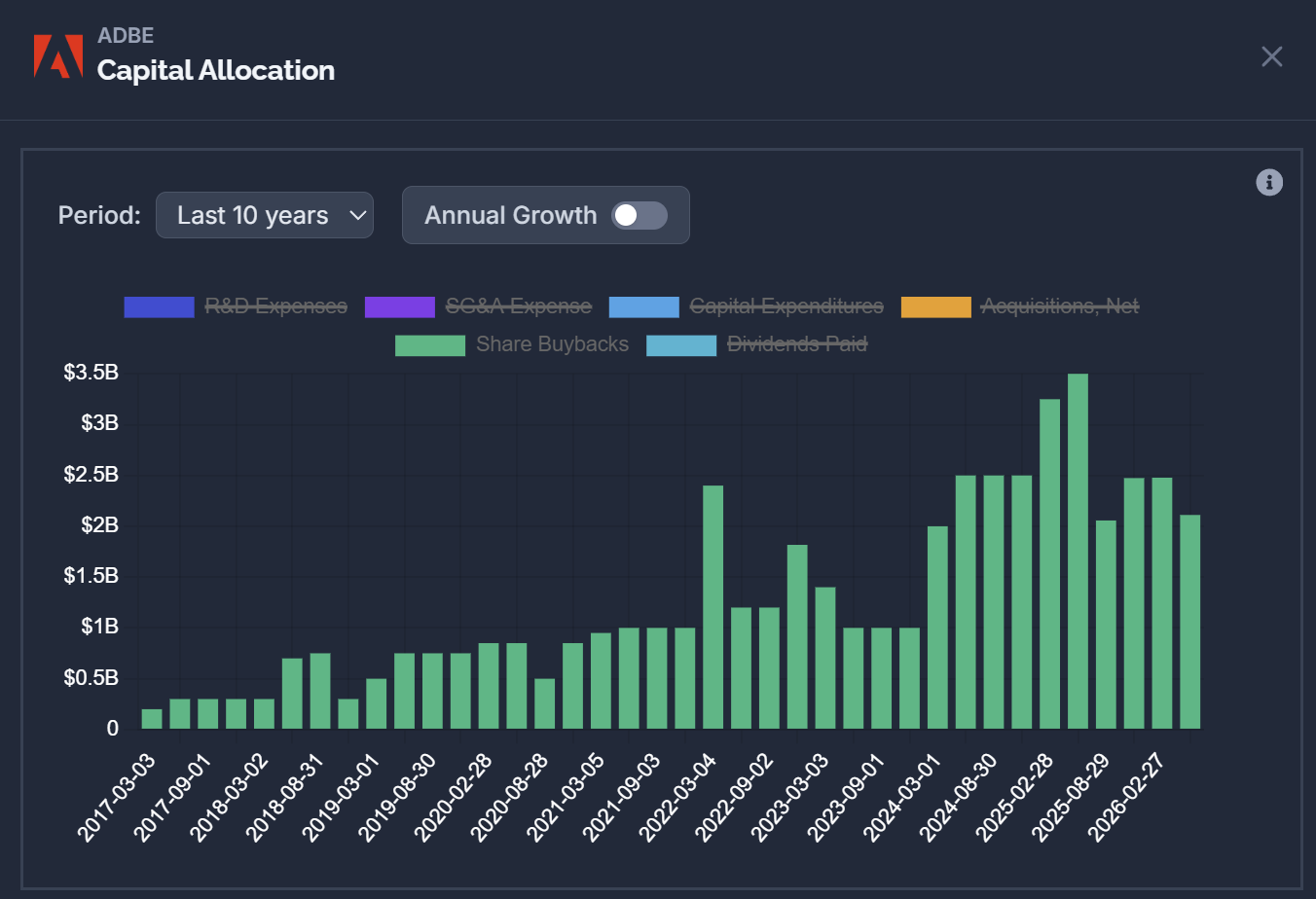

Adobe’s management clearly recognizes this and continues repurchasing shares aggressively.

During Q2 alone, Adobe repurchased approximately 8.5 million shares and still has roughly $27 billion remaining under its authorization. These buybacks are occurring at such a scale that Adobe reduced its diluted share count by 2.2% in a single quarter. Year-over-year, diluted shares outstanding declined from 429 million to 402 million, a reduction of 6.3%.

Last quarter, I said Adobe traded at a dirt-cheap valuation. If that was dirt-cheap, I do not know what to call the valuation today, but let’s just call it “cheaper than dirt-cheap.”

I am strongly considering adding to my Adobe position and will notify paid subscribers if I do.

Until next time,

Lucas

Summit Stocks

Disclaimer: the information provided is for informational purposes only and should not be considered as financial advice. I am not a financial advisor, and nothing on this platform should be construed as personalized financial advice. All investment decisions should be made based on your own research.

I agree the distribution moat is real, but I still think Adobe’s weakest customer relationship is pricing.

The product is embedded, but it is also expensive. That is where AI-native tools can create pressure: not by replacing every workflow overnight, but by making customers question how much of the Adobe bundle they actually need.

Worse case scenario, should the share price go even lower, and more board members leave their leadership positions, expect a bigger company (maybe Anthropic) or private equity make an attempt to buy the company in whole or part to get their hands on the distribution network.